Update: Nov '21 Observations

Omicron Pivot is a convenient narrative to explain the November sell-off, but risk assets were probably due for a decline after solid earnings season gains...

Observations & Performance: November 2021

November finished on a down note for most global risk assets. US equities were grinding higher for most of the month as the corporate earnings season delivered another quarter of solid growth; S&P 500 profits for Q3 increased ~40% year-over-year. In addition, most economic indicators have been showing improvement. Thus, economic and corporate fundamentals remain positive and up-trending.

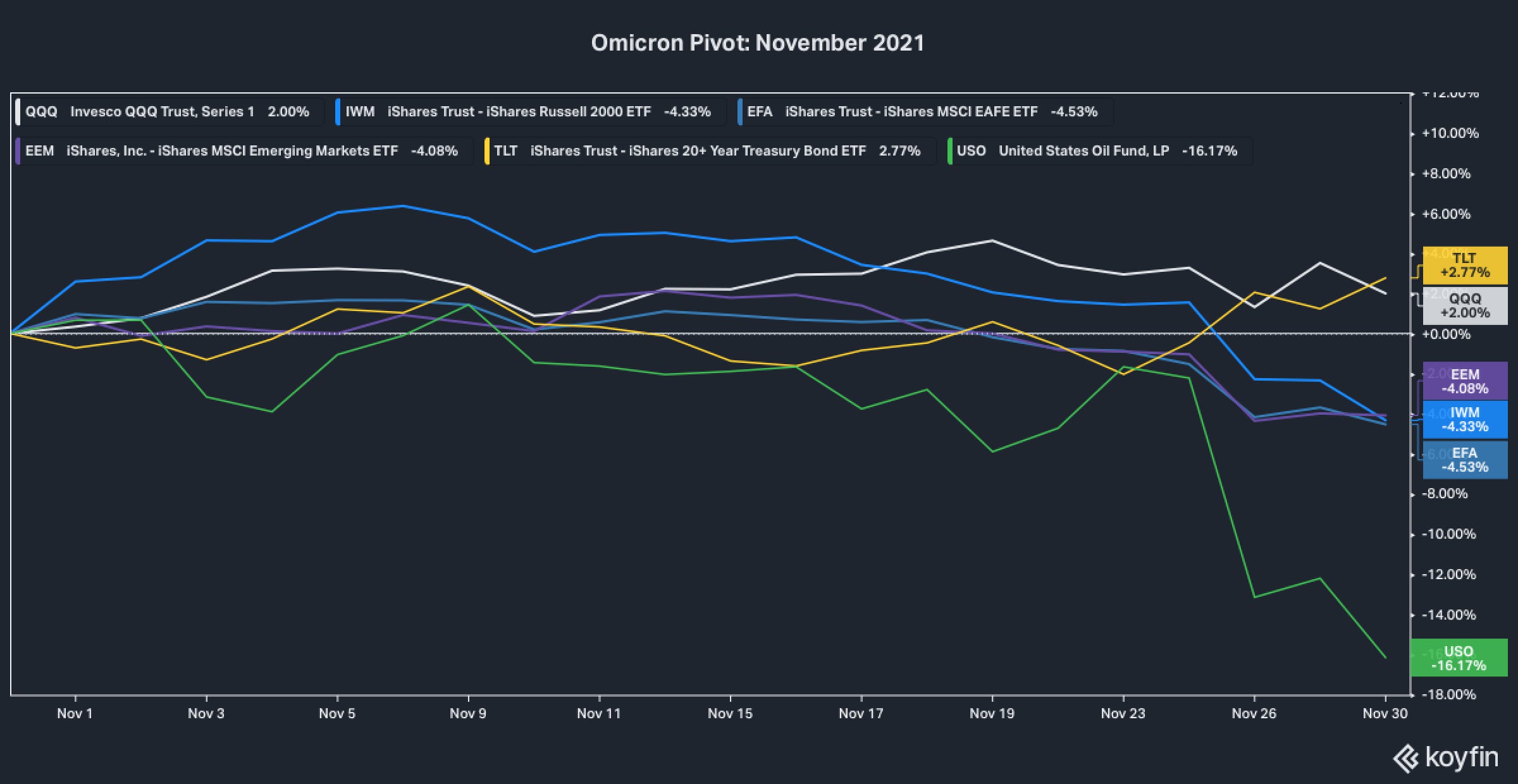

But reports of a new COVID variant (Omicron) emerged last week and risk assets abruptly declined. Call it the Omicron Pivot. Apparently, Omicron was first detected in July in South Africa where case counts have been increasing ever since. But when Omicron cases were discovered in Europe, Japan, and elsewhere, policymakers there were prompted to announce new travel/movement restrictions. This negatively impacted the so-called “epicenter” assets and regions — energy, commodities, travel-related businesses, various services industries, and other broadly-defined cyclical/value assets — especially in non-US markets.

We suspect the panic headlines are overdone and the severity of the virus will be mild and/or treatable for the vast majority of the population — as we have witnessed with the Delta variant. Regardless, time and data will bring clarity.

Without indications that COVID is becoming more severe, we observe no willingness, nor a large enough consensus, to endure more expansive/intrusive restrictions in the US…

In the US, the population has mostly adapted to community life with the virus, concluding the COVID threat is limited. Without indications that COVID is becoming more severe, we observe no willingness, nor a large enough consensus, to endure more expansive/intrusive restrictions in the US, although certain one-off communities might take a more cautious approach. To the extent the US economy is reasonably self-sufficient, growth most likely continues at an above-trend pace into 2022. Moreover, Fed Chair Powell’s testimony to Congress on 11/30 confirmed FOMC intentions to accelerate the pace of “tapering” asset purchases; it’s doubtful the Fed would move ahead with such “monetary tightening” plans if Omicron were viewed as a serious growth threat. At this point, it is not. In fact, Powell’s stance might eventually be viewed as a positive, indicating the Fed sees persistent growth ahead despite the virus.

Omicron might be just a convenient narrative to which the recent sell-off is being attributed — the catalyst for a much needed pause, profit-taking episode, or portfolio risk rebalancing.

Otherwise, equities and other risk assets were probably due for a sell-off as part of the normal ebb and flow of the global capital markets. Frankly, this should not be overlooked. Simply put, Omicron might be just a convenient narrative to which the recent sell-off is being attributed — the catalyst for a much needed pause, profit-taking episode, or portfolio risk rebalancing. Moreover, we suspect temporary technical factors contributed to the late November declines. For a more lengthy discussion on non-fundamental and technical factors, please refer to our Weekly Briefing from 11/28/21.

To summarize high-level asset class performance for November:

S&P 500 (SPY) was up over 2% for November before the Omicron Pivot erased all the gains. SPY finished with a decline of -0.8%. Non-US markets showed larger declines as movement restrictions potentially threaten economic activity. Developed Markets (EFA) and Emerging Markets (EEM) declined -4.5% and -4.1%, respectively.

Cyclical/value and related themes underperformed on growth concerns and falling interest rates — but “enduring” secular growth equities outperformed. For instance, Russell 2000 (IWM) declined -4.3%, but the Nasdaq 100 (QQQ) gained 2.0%. Indeed, quality large-cap US growth companies tend to deliver defensive attributes in periods where global growth comes into question. Similarly, Energy and Financials underperformed with losses in November, but Technology and Consumer Discretionary delivered gains (see US/Global Equities below).

Long-duration safe-haven USTs also outperformed in November, delivering “crisis alpha” along with the US dollar. UST 20+ Year (TLT) gained 2.8% and the US dollar (USDU) gained 1.7% versus a basket of foreign currencies (33% Euro).

Energy commodities epitomize the epicenter of the sell-off since travel by road/air accounts for so much energy consumption. WTI Crude (USO) declined -16.2% in November.

Sources: CCM, Koyfin

Sources: CCM, Koyfin

Sources: CCM, Koyfin

We deliver timely and relevant data/insights, but in the new year our best content will be available ONLY to paid subscribers. For full access to Coffee & Capital Markets, please consider joining our community as a paid subscriber.

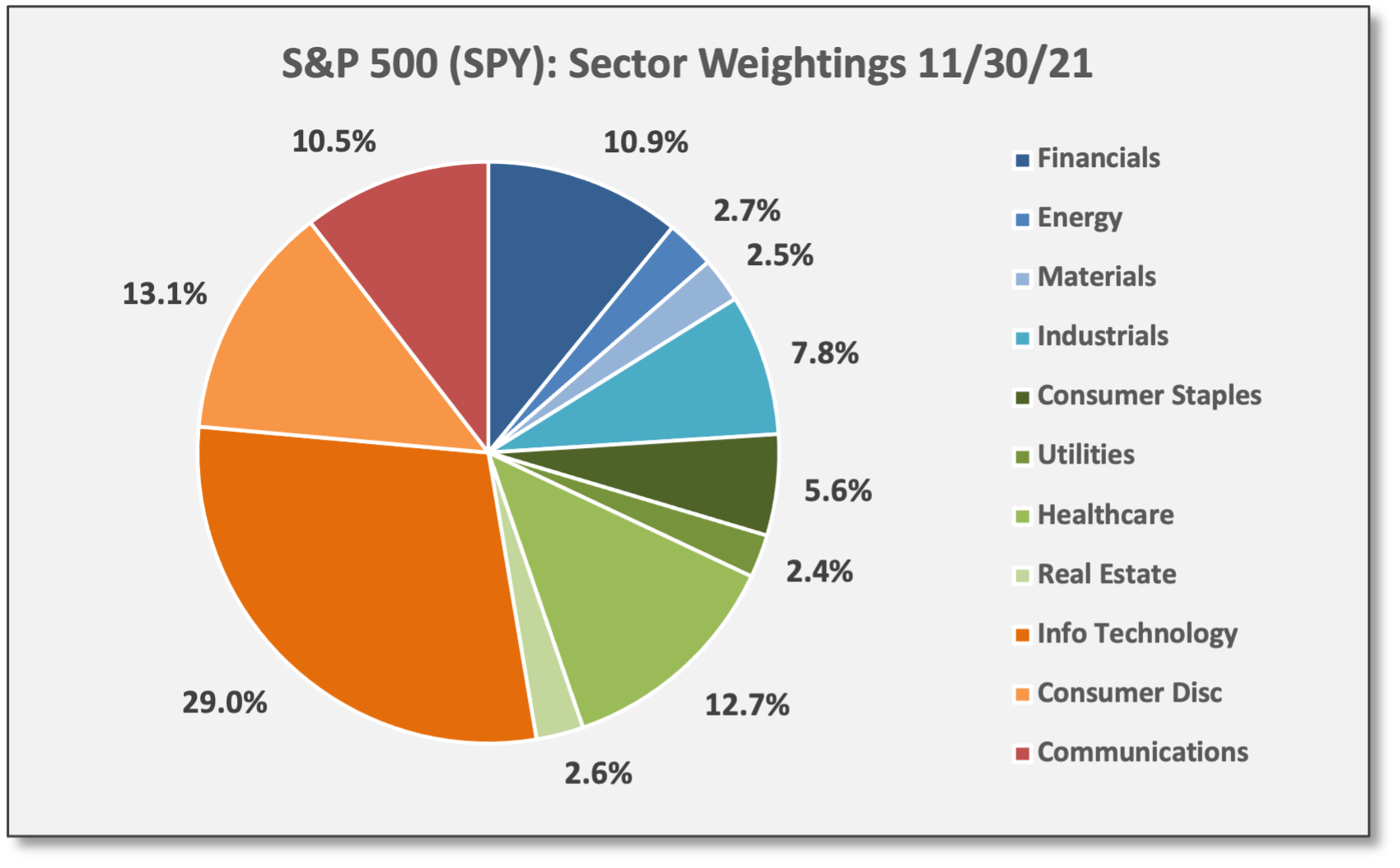

US/Global Equities

US equities declined in November, but outperformed non-US markets where travel/movement restrictions were announced. Cyclical/value underperformed, but quality/secular growth outperformed with gains for the month.

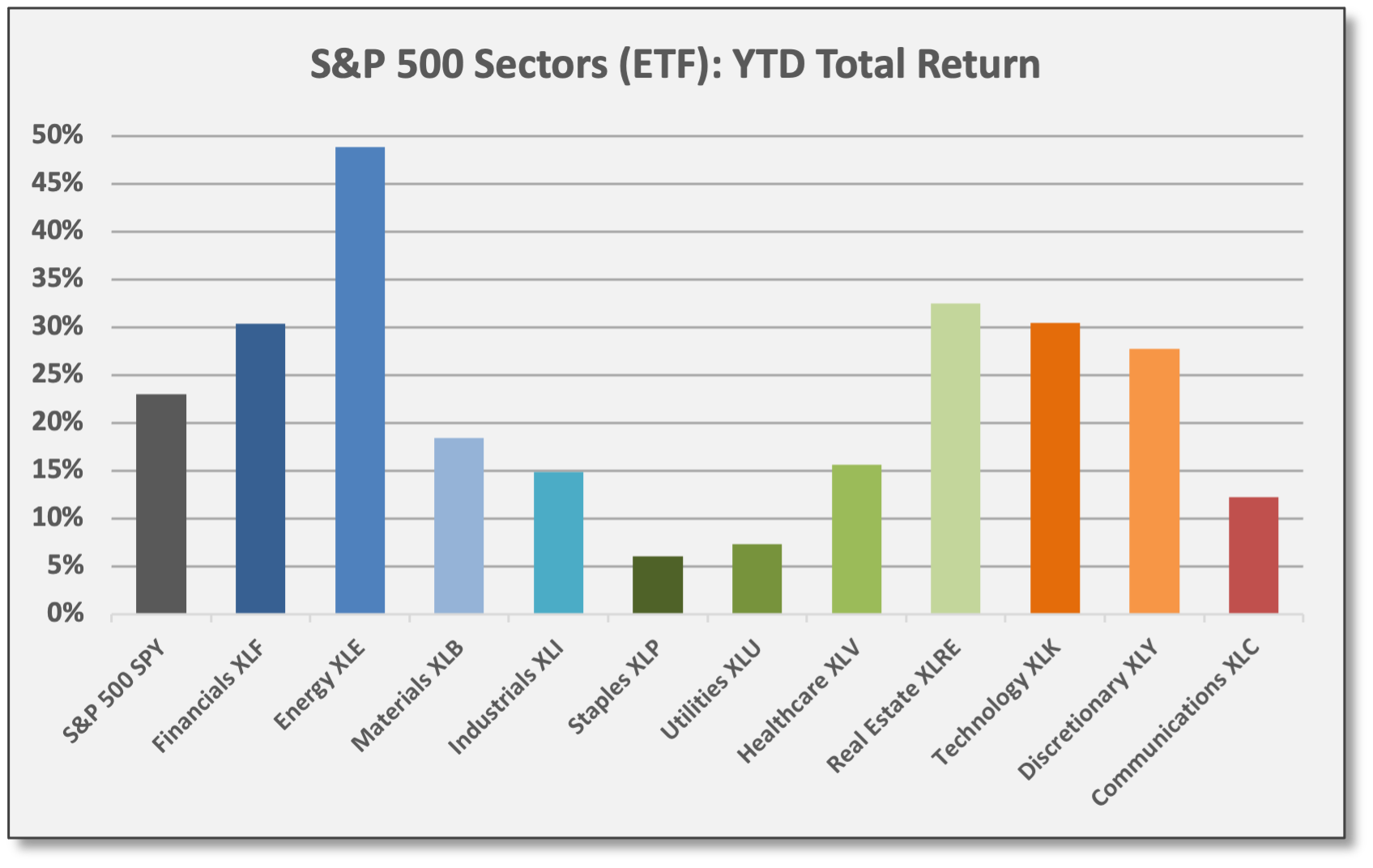

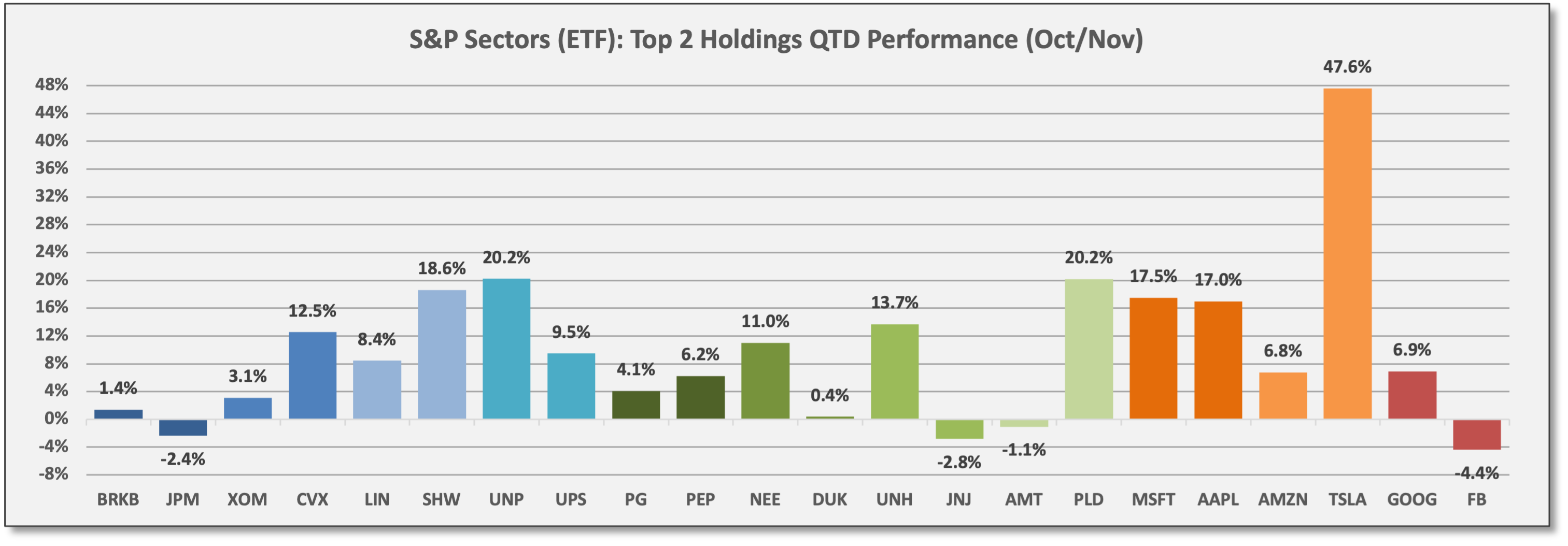

Energy (XLE) and Financials declined -5.7% and -5.0% in November, respectively. Energy remains the top performing sector for 2021.

Technology (XLK) gained 4.5% in November. Apple (AAPL) gained 10.5%. Quality/secular growth sectors are mostly outpacing for Q4.

Defensive/yield-oriented sectors (Staples, Utilities, Healthcare) declined in November and are mostly lagging in 2021. Real Estate (XLRE) is the exception, but the sector, historically perceived as a yield provider, actually has ample growth exposure tied to digital communications.

Sources: CCM, Koyfin

Sources: CCM, Koyfin

Sources: CCM, Koyfin

Sources: CCM, Koyfin

Sources: CCM, Koyfin

Sources: CCM, Koyfin

Sources: CCM, Koyfin

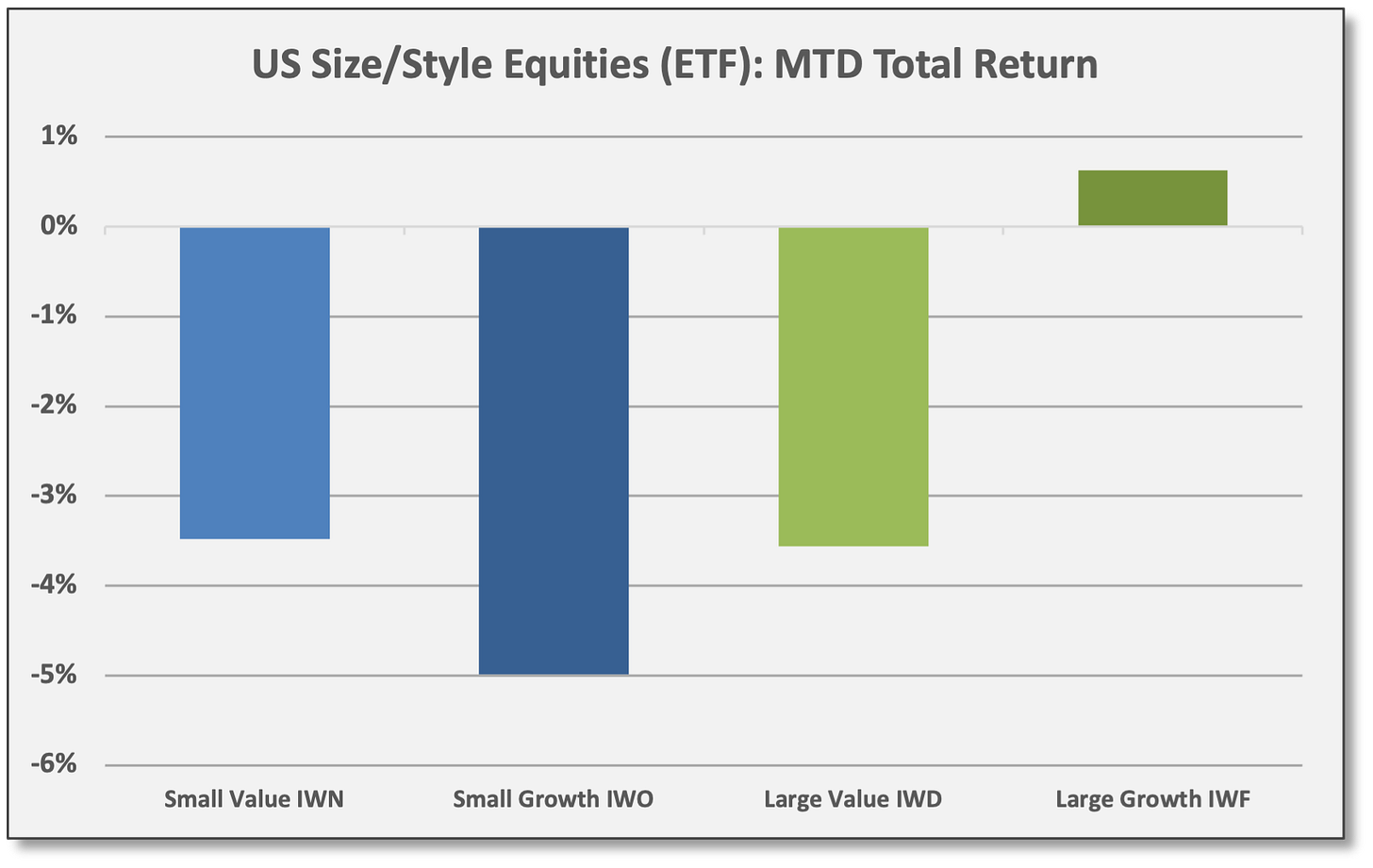

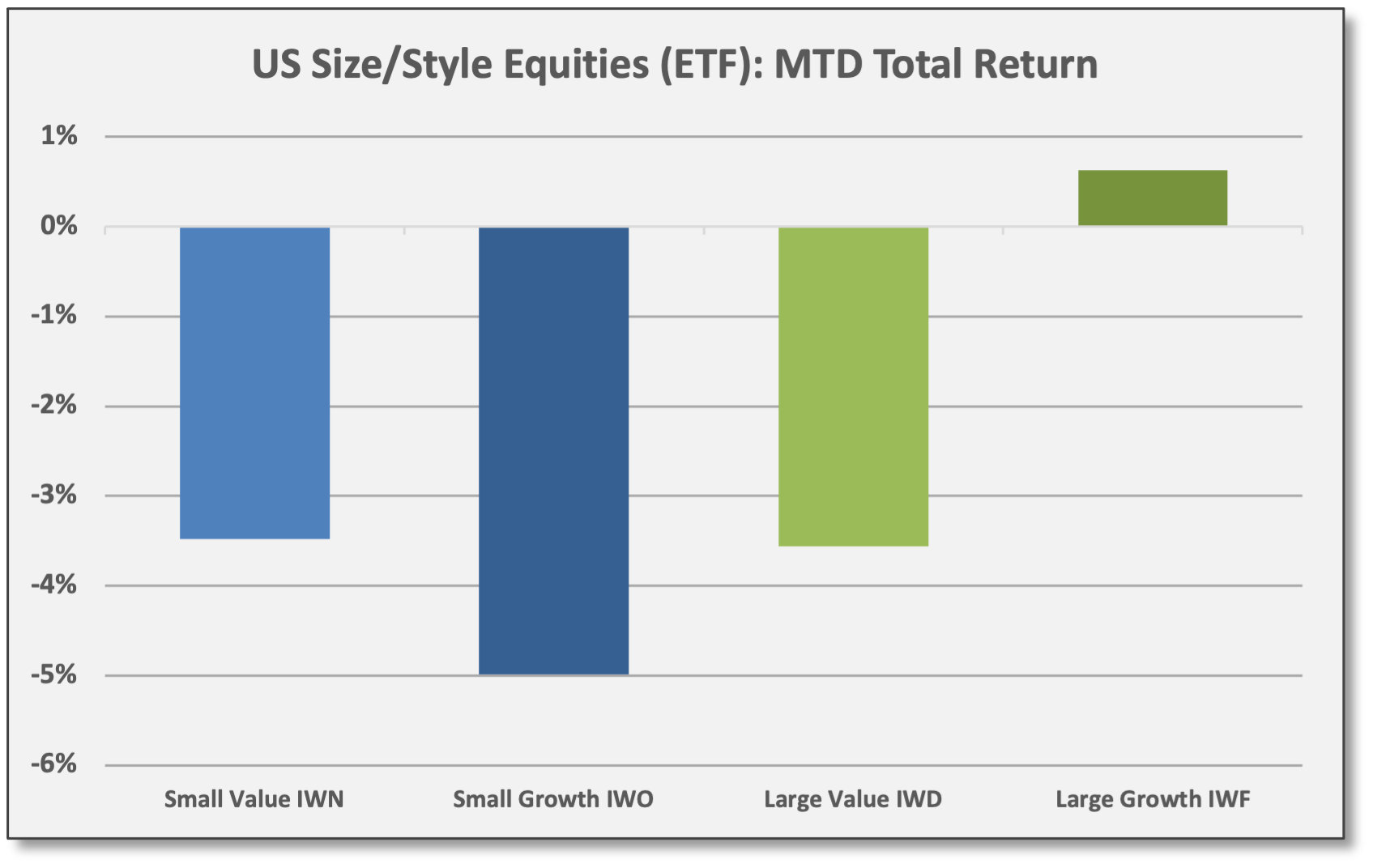

Sources: CCM, Koyfin Large-cap growth delivered “defensive” positive returns in November.

Small-cap struggled in November as a cyclical proxy (both value and growth). For 2021, small-cap value has delivered strong gains due to Financials and Energy.

Sources: CCM, Koyfin

Sources: CCM, Koyfin

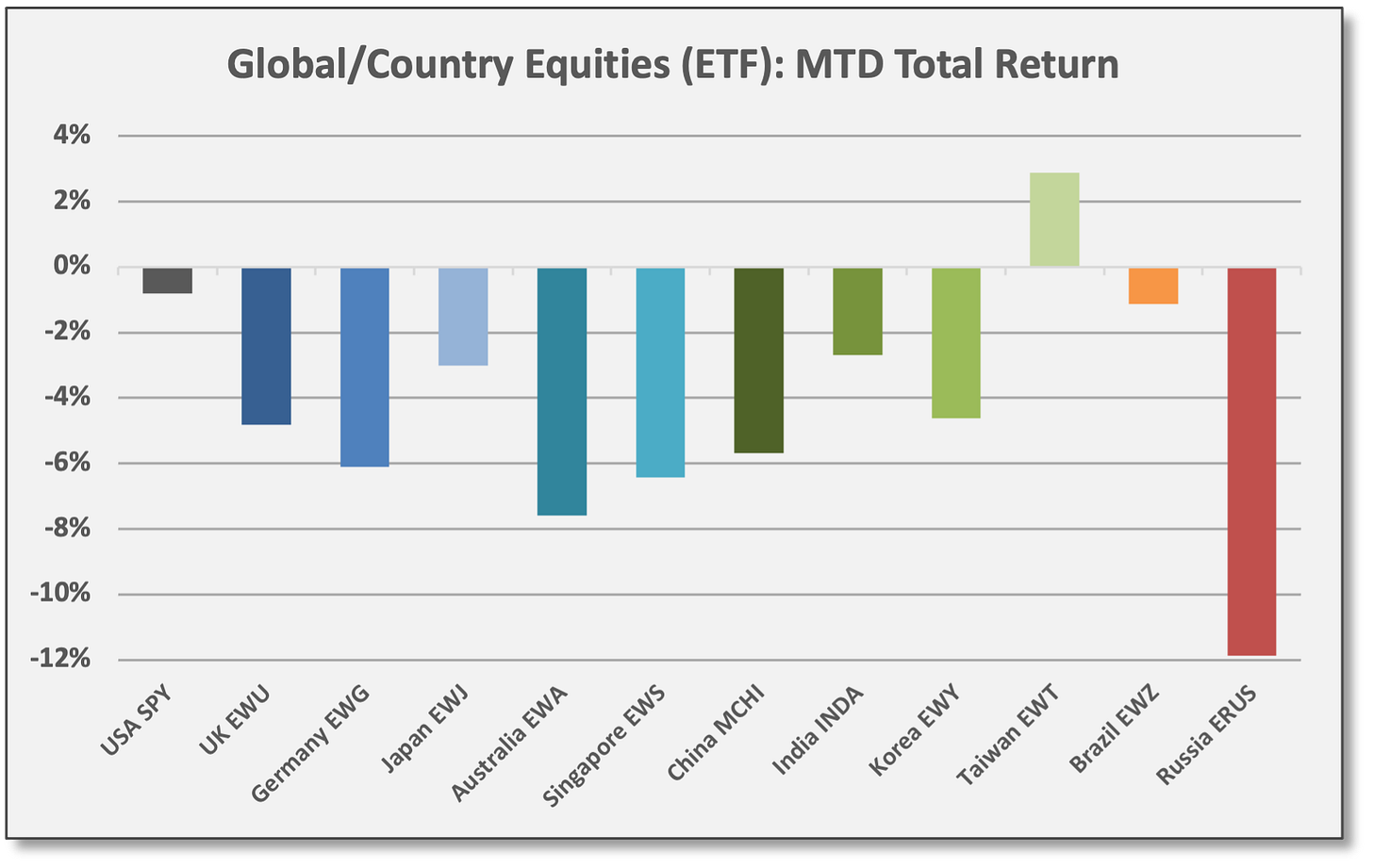

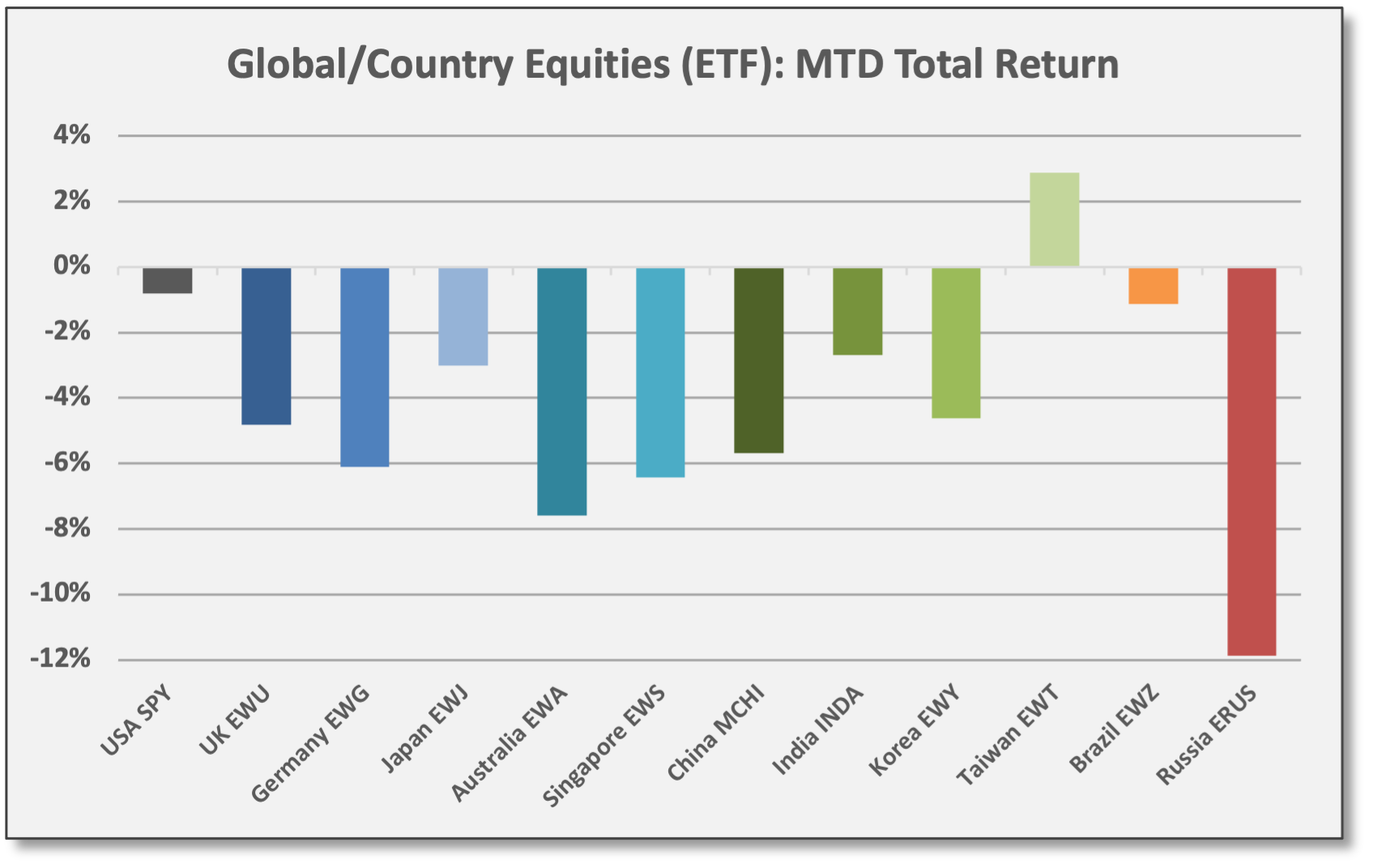

Sources: CCM, Koyfin In November, non-US markets declined across the spectrum. Russia underperformed due to its concentrated energy exposures.

For 2021, the US has consistently outperformed. For non-US markets, performance for 2021 shows wide dispersion across markets.

Sources: CCM, Koyfin

Sources: CCM, Koyfin

Sources: CCM, Koyfin

Fixed Income & Credit

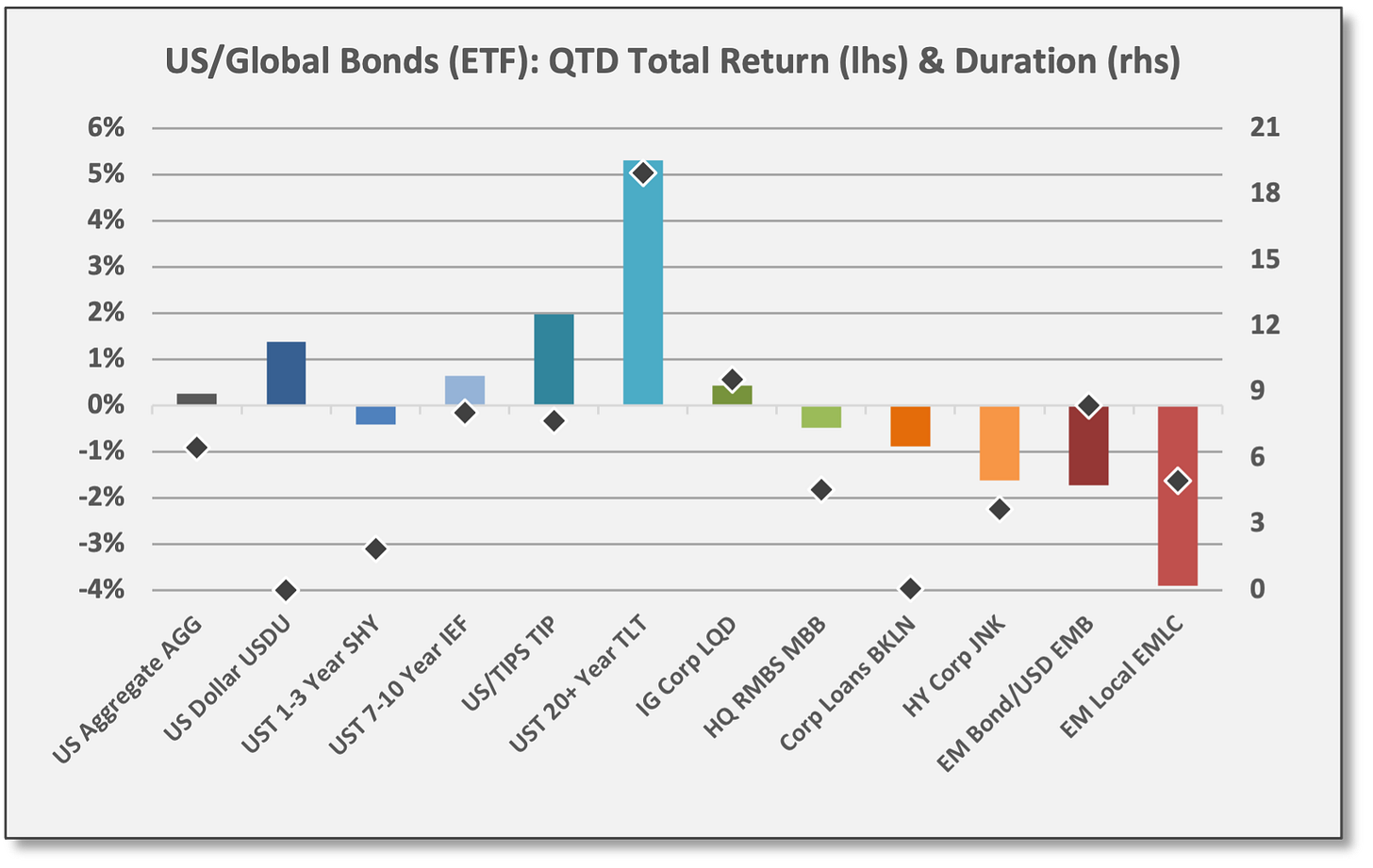

Interest rates were grinding steadily higher in November until the Omicron Pivot threw that move into reverse. Leading up to Thanksgiving, bond investors were pushing rates higher, assuming a more aggressive Fed Policy shift (faster “tapering” of asset purchases and sooner rate hikes), but the COVID headlines resulted in a risk-off rotation that benefitted high-quality bonds. The UST 10-year closed November with a yield of 1.43%, down from a pre-holiday level of 1.64% and down 12 basis points for the month.

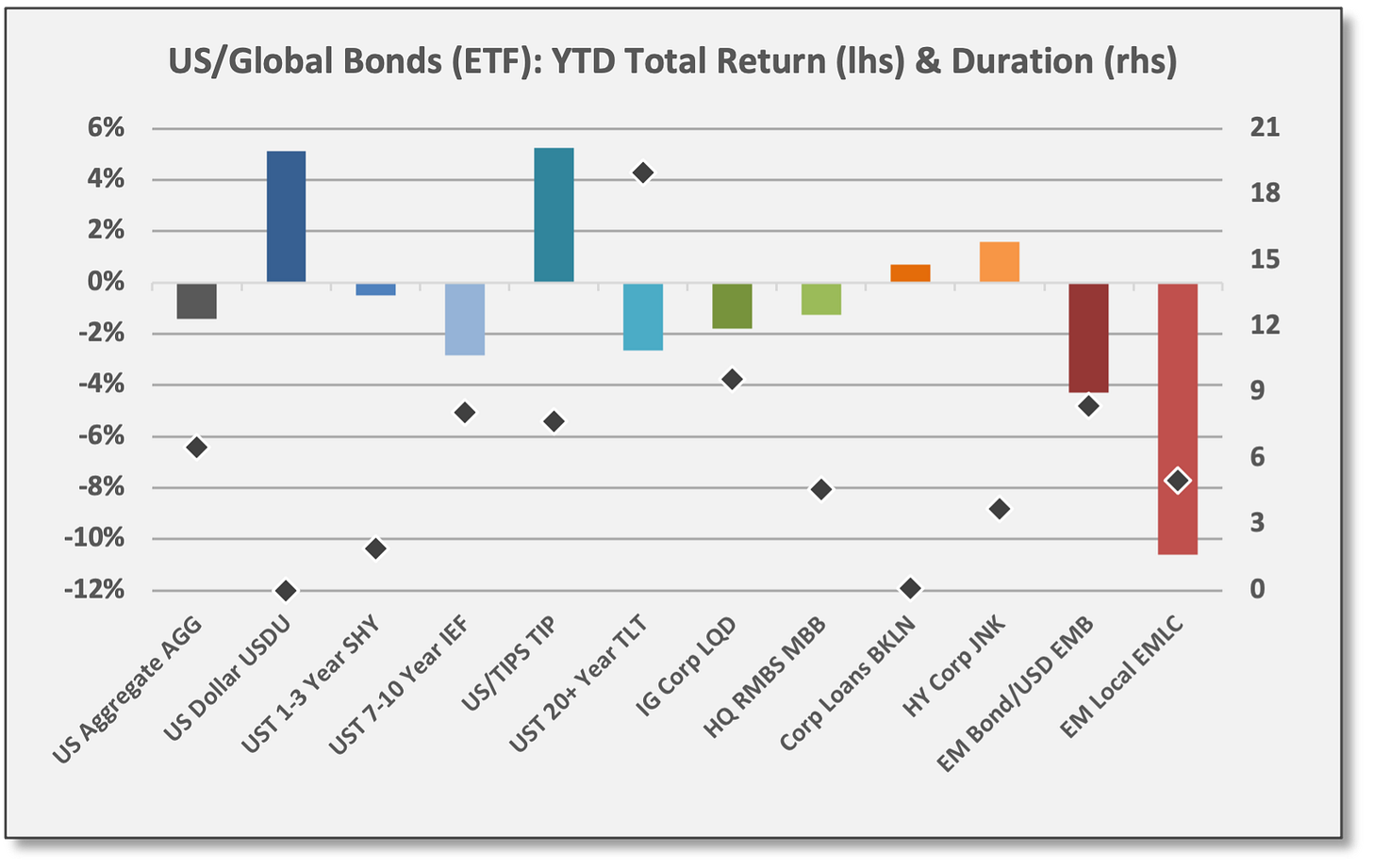

UST 20+ Year (TLT), with a duration of 19.0 years, gained 2.8% for November. Intermediate and inflation-protected USTs also gained due to rate duration. For 2021, TIPS have outperformed due to rising inflation, but long-duration USTs have declined with rates moving higher for the year.

US Aggregate Bond (AGG) gained 0.3% for November. USTs gained, but investment-grade corporate bonds and mortgage-backed securities declined modestly for the month with wider credit spreads. For 2021, the AGG is down -1.4%.

Spread strategies underperformed in November. High-yield corporate bonds (JNK) declined -1.3% with HY credit spreads widening ~40 basis points to +353 (as of 11/29). HY bonds/loans have delivered modest gains for 2021.

Sources: CCM, Koyfin

Sources: CCM, Koyfin

Sources: CCM, Koyfin

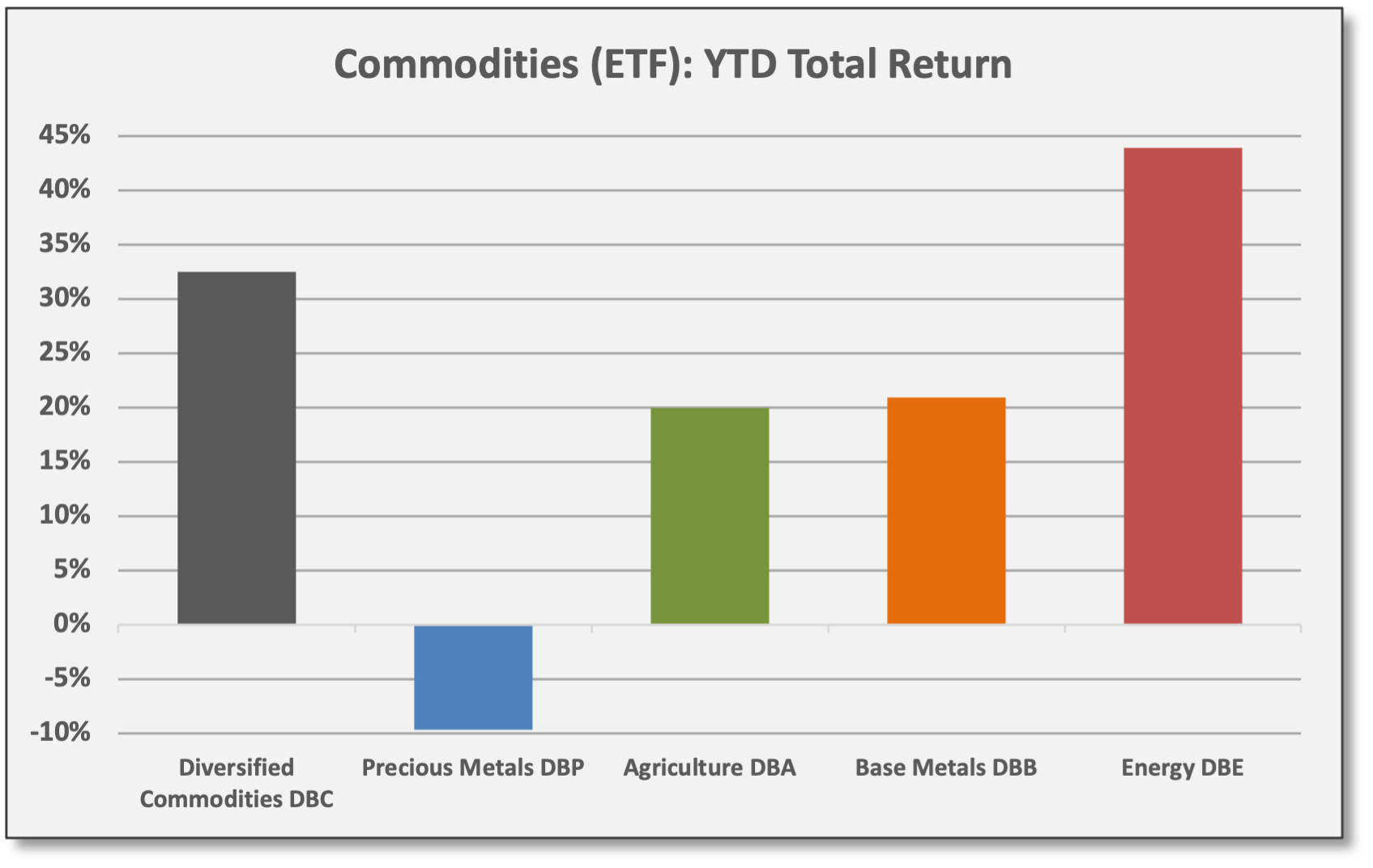

Commodities & Real Assets

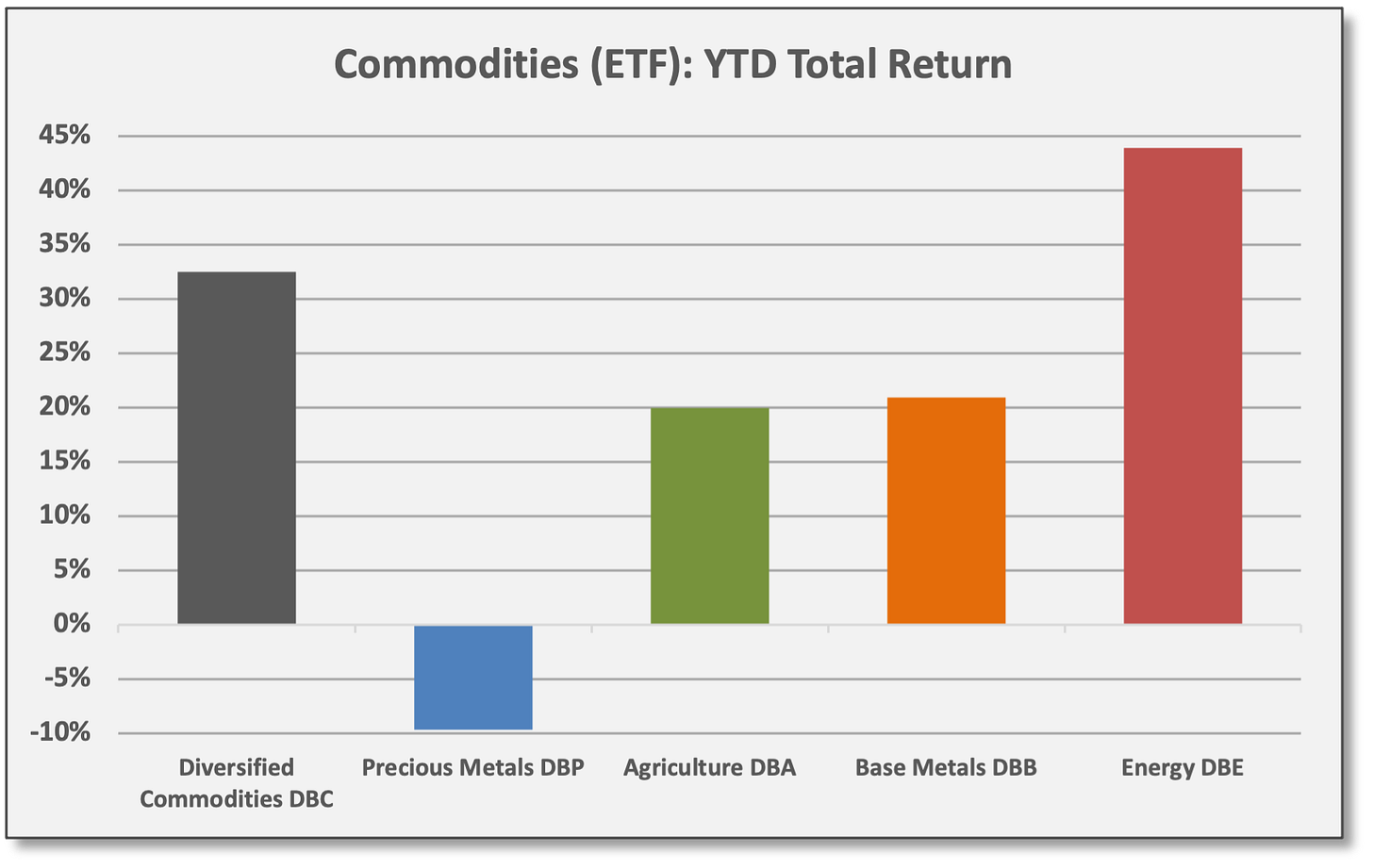

Energy commodities epitomize the epicenter of the sell-off since travel by road/air accounts for so much energy consumption. Thus, energy commodities suffered sharp losses in response to the Omicron Pivot.

Energy (DBE) declined -14.5% for November. WTI Crude closed at 67.53 per barrel. Energy remains the top performer for 2021, but gains mostly were achieved in the first half of the year.

Other growth-sensitive commodities underperformed in November with Base Metals (DBB) down -2.6%.

Precious Metals (DBP) failed to deliver meaningful protection in the sell-off, declining -1.5%. SPDR Gold (GLD) was down -0.7% for November. Gold has failed to deliver as an inflation hedge this year.

Sources: CCM, Koyfin

Sources: CCM, Koyfin

Sources: CCM, Koyfin