Update: May '22 Observations

Weakness in housing and employment could help alleviate inflation, bringing us closer to an eventual Fed policy pivot...

Observations: May 2022

“April showers bring May flowers,” but in the case of the US economy and equity markets, April fears were reasonably validated by weaker growth data reported during the first several weeks of May. In fact, the storm clouds were growing darker, but late in the month, early signs of capitulation emerged and markets rallied.

This remains the dominant narrative for May despite the mood being tempered by equity losses in the final post-holiday trading session of the month.

As we enter June, investor sentiment remains negative. Before sentiment improves in a lasting way, investors are scanning the data for positive catalysts in three main areas: (1) peaking inflation, (2) an “end in sight” for Fed Policy, and (3) relative stability in economic and corporate fundamentals to ensure a severe growth slowdown is averted. Conditions are far from definitive, but early hints of progress have emerged on all three fronts.

Key takeaways from data points reported in May:

Housing activity is slowing amid higher mortgage rates. Supply/demand conditions support further growth, albeit at a slower pace due to rates.

Employment conditions might be easing, reducing wage pressures.

Financial conditions continue to tighten amid Fed Policy, rising interest rates, wider credit spreads, and a stronger US dollar.

Manufacturing/Services activity continues to decelerate, but still shows expansionary growth.

GDP for Q1 was negative and revised lower in May, but resilient consumer spending is stable at the least — and might be improving.

Inflation metrics are showing early signs that inflation has peaked.

Housing: Higher mortgage rates are impacting housing activity. Existing home sales declined 2% in April (reported in May) and are down 14% from January levels. New home sales declined 17% in April and are down 30% versus December. Housing starts declined in April along with new building permits. Across the US, 30-year fixed mortgage rates are 5.4%, down from peak levels of 5.6% in recent weeks as rates have traded lower, but still elevated for 2022 since the Fed launched its tightening program.

Employment: In early April, weekly jobless claims dropped to a 54-year low of 168,000, but claims have moved higher since with the latest reading at 210,000. The four-week moving average has increased from 170,500 in early April to 206,750 as of 5/21/22. Some of the increase is due to arcane seasonal adjustments, and the increase is not too alarming, but the direction (up) is clear and that deserves attention. Despite a jobless rate at 3.6% — compared to a pre-COVID low of 3.5% — non-farm payrolls (NFP) payrolls are lower by 1.2 million jobs versus February 2020; the Labor Force Participation Rate (LFPR) has dropped to 62.2% versus a pre-COVID 63.4% as workers either retired or left the work force for other reasons. So, the supply of labor has been reduced, but other factors suggest supply/demand conditions could be shifting, thereby reducing marginal wage pressures: (1) Indeed.com reports reduced job postings, (2) retired workers could rejoin the labor force due to higher inflation and living expenses, and (3) overstaffed companies could implement layoffs, including software firms facing tighter conditions (i.e., “unprofitable” tech companies). Already, layoffs have been announced at Netflix, Carvana, Ford, and others with layoffs reportedly being considered at Amazon and Wal-Mart.

Financial Conditions: To date, the current FOMC regime has enacted rate hikes on just two occasions — 25 basis points in March of this year and 50 basis points in May. For June and July, successive hikes of 50 basis points are expected, presumably lifting the Fed Funds rate from 1.00% to 2.00%. Effectively, Fed Policy would remain accommodative since 2.00% is below the prevailing inflation rate and below the Fed’s stated neutral policy rate (2.40%). With FOMC meetings scheduled for September, November, and December, the Fed will no doubt continue to hike rates over the balance of 2022, so the Fed Funds rate could approach 3.00% by year-end. However, market-based factors have already tightened financial conditions. Primarily, these include UST interest rates, credit spreads, and foreign exchange rates: So far this year, (1) UST 2-year and 10-year rates have increased ~180 bps and ~135 bps, respectively; (2) high-yield corporate credit spreads have widened ~110 bps to + 419; (3) US dollar has strengthened over 4% versus a basket of foreign currencies.1 For US corporations, all these add to cost structures.

Manufacturing/Services: ISM Manufacturing missed estimates and dropped to 55.4 in April, while Services also missed and dropped to 57.1. Both measures are lower versus a year ago, although both continue to signal a growth expansion. S&P Global “flash PMI” surveys showed further deceleration in May for both manufacturing and services. Separate reports from the NY Fed and Philadelphia Fed also pointed to manufacturing deceleration. Ideally, the economic growth expansion continues, but at a less inflationary pace.

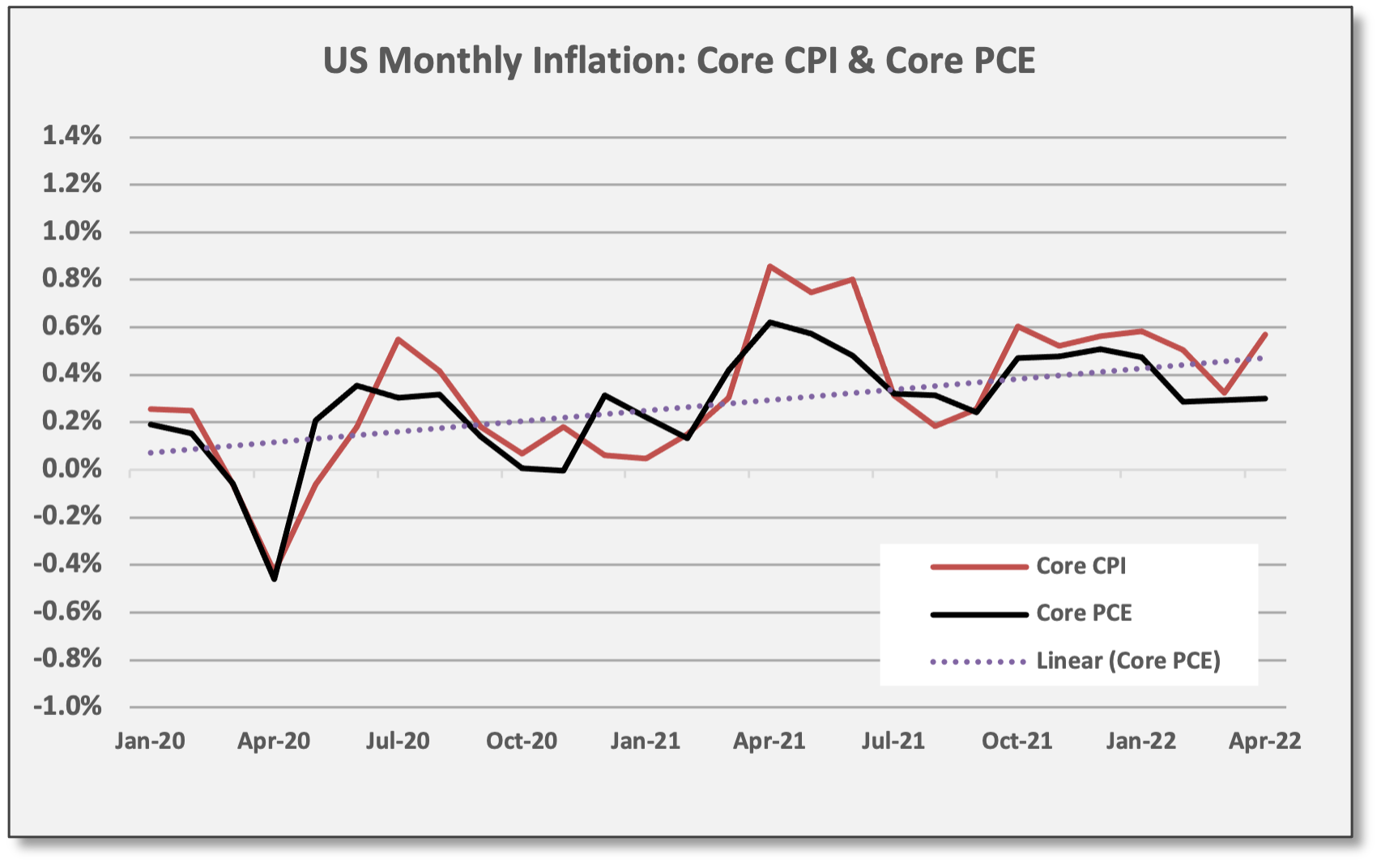

Inflation: Has inflation peaked yet? Various metrics suggest this might be the case, but more time and data points are needed to confirm. Headline CPI and PCE for April both showed declines. Core inflation metrics — excluding volatile food and energy prices — have been lower overall, but show less pronounced improvement. Inflation remains up-trending since early 2020 when COVID policies disrupted supply/demand conditions — policy decisions were the pre-cursor to the inflation spike (see graphs below). Until COVID-related inflation trends inflect lower, we suspect the FOMC will continue hiking interest rates, but with each passing month, we are getting closer to a policy pivot. As an aide, trailing one-year core inflation was 6.2% for Core CPI and 4.9% for Core PCE, but these one-year rates include past readings at much higher levels. Presumably, “sequential” core inflation tracking in the 0.2% to 0.4% range per month — over a series of months — is an important marker to achieve before the FOMC builds internal consensus for taking a less aggressive approach.

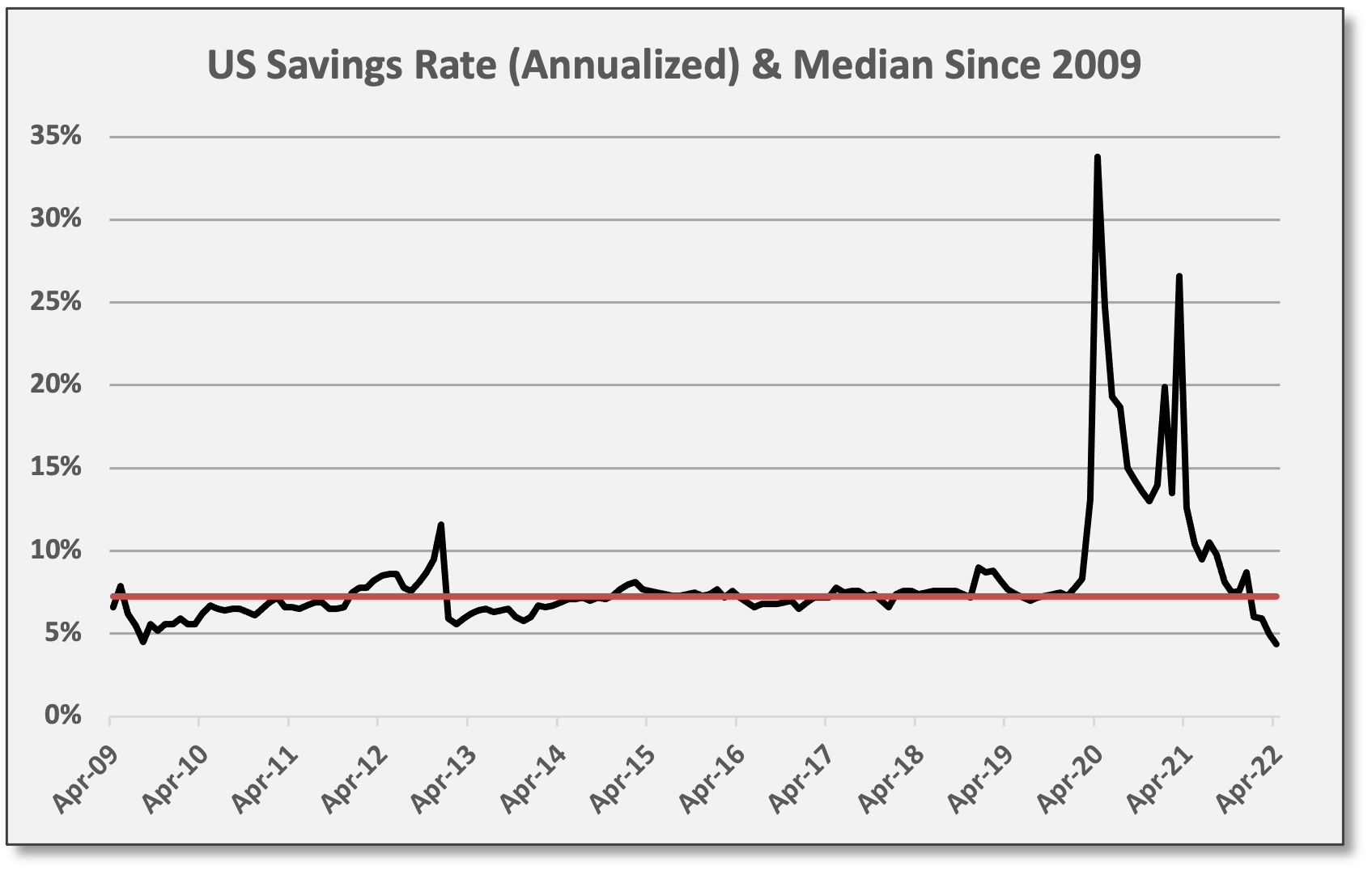

GDP & Retail Sales: In late May, GDP for Q1 was revised lower to negative 1.5% growth. Hence, the US economy is halfway to an economic recession based on the technical definition of two consecutive quarters of negative GDP growth. However, Q2 indicators point to improved growth activity — the Atlanta Fed GDPNow model is estimating Q2 GDP at positive 1.9%; even factors inside the Q1 GDP report were encouraging. For instance, personal consumption was revised higher to a 3.2% annualized growth rate. Consumption accounts for ~65% of US GDP. The largest detractors in Q1 were government spending and exports, the latter reflecting a strong US dollar and weak conditions in non-US markets. In other words, GDP struggled in Q1, but core domestic consumption is on solid footing. Moreover, retail sales increased 0.9% in April with positive revisions to prior months. Even though retail sales are being boosted by inflation — higher prices, but not necessarily higher volumes — sales have actually accelerated over the last six months. In addition, consumer financial positions remain solid (in aggregate) due to strong balance sheets and rising wages. Granted, consumers have tapped their savings to support recent spending in the face of higher prices (inflation). The savings rate just dropped below 5% for the first time since 2009, but even with lower saving rates, financial obligations relative to disposable income remain at the lowest levels in over 40 years (see graph below). Eventually, inflation levels will move lower as supply conditions normalize, but higher wages should provide lasting benefits to consumers and the crossover point — where trailing one-year inflation goes below wage gains — could occur within 6-12 months, according to JPMorgan.

Corporate Earnings: Q1 corporate earnings season stretched over April/May and is virtually complete. For the S&P 500 Index, 75% of reporting companies beat bottom-line EPS estimates by an average margin of ~4% and a median margin of ~8%. For Q1, EPS increased ~9% versus a year ago. Notably, EPS for the Energy sector increased 276%. Excluding Energy, EPS for the S&P 500 increased 3% versus a year ago. As we enter June, EPS for the S&P 500 for CY‘22 are now estimated to increase ~10%. On a top-line basis, 71% of reporting companies beat REVENUE estimates by an average margin of ~3% and a median margin of ~2%. For Q1, REVENUES increased ~14% versus a year ago. As we enter June, REVENUES for CY‘22 are estimated to increase ~10%.

Are housing and employment conditions moderating? Housing and labor are two areas of concern for the Fed because price trends from these market segments are considered sticky, persistent, and enduring. If price levels reach troublesome levels, negative effects could be long-lasting. At least, that is the operating theory for the Fed’s policy decisions.

How directly Fed Policy actually impacts these factors is debatable and even Fed Chair Powell admitted the Fed’s tools are blunt instruments.

“Weakness” in housing and labor — or simply a slower pace of growth that is less inflationary — should lead to lower price inflation.

One thing seems clear: “Weakness” in housing and labor — or simply a slower pace of growth that is less inflationary — should lead to lower price inflation. When that happens, the Fed should be that much closer to reaching its “price stability” objective. “Peaking inflation” is a catalyst investors are hoping to see and housing and employment are two early indicators that will influence future inflation.

Fed Mission: Reduce Growth. It seems problematic, no matter how painful inflation might be, but reducing economic growth is the overt strategy being outlined by the Fed. At a Wall Street Journal event on 5/17/22, Fed Chair Powell made it clear: “This is not a time for tremendously nuanced readings of inflation. We need to see inflation coming down in a convincing way. Until we do, we’ll keep going.”

“There could be some pain involved to restoring price stability.” Jerome Powell, Fed Chair, 5/17/22

Later, Powell outlined the Fed’s process: The Fed raises interest rates, which makes financial conditions tighter, which eventually impacts the economy by reducing growth. Unequivocally, Powell said the mission of the Fed is to “slow growth” because the Fed believes this is needed to reduce inflation. Powell added: “There could be some pain involved to restoring price stability.”

As noted above, markets anticipate rate hikes of 50 bps in June and July. Subsequent hikes over the balance of the year could put the Fed Funds rate at 3.00%. By comparison, the Fed maintains a target core inflation level of 2% and defines neutral policy rates at 2.40%. In other words, policy will be restrictive by year-end, not to mention the planned shrinking of the Fed’s balance sheet. As stated earlier, real-time market-based factors have already been doing the Fed’s work — tightening financial conditions aggressively.

“It may make sense to pause in September, depending on the economy.” Raphael Bostic, Atlanta Fed President, 5/23/22

To reiterate, for the Fed to consider a meaningful policy pivot, a series of monthly data points showing inflation heading lower is needed. This might happen sooner than expected. In light of tighter financial conditions, Atlanta Fed President Raphael Bostic hinted that the Fed might reduce the pace of rate hikes by September (i.e., hikes of 25 bps). At the Rotary Club of Atlanta on 5/23/22, Bostic said: “It may make sense to pause in September, depending on the economy.”

In the meantime, we monitor housing and employment for signs of deceleration. This Friday 6/3 brings the non-farm payrolls report for May. Monthly NFP data is notoriously subject to revision, but the May report will be the first print since jobless claims turned higher and several corporations announced layoffs. All this makes the upcoming jobs report even more important than usual.

Cross-Asset Performance: May 2022

What drove markets higher in late May? For starters, equity markets were deeply oversold and short-term rallies often occur in down-trending bear markets. Thus, technical conditions were ripe for a move higher. Adding to the upside move for equities were (1) monthly rebalancing flows from balanced mutual funds, (2) short-covering by momentum strategies, (3) corporate share repurchases and insider-buying activity, and last but not least, (4) short-gamma conditions which prompted share buying by options dealers for delta-hedging purchases; short-gamma always amplifies price movements in either direction, although conditions are now relatively neutral.

US equities surged over the final seven sessions of May, lifting the S&P 500 (SPY) to a modest positive return for the month. SPY gained 0.2% in May but is down -12.8% for 2022. Growth-oriented shares once again lagged: Nasdaq 100 (QQQ) finished down -1.6% and is down -22.4% for ‘22. Non-US equities delivered gains in May.

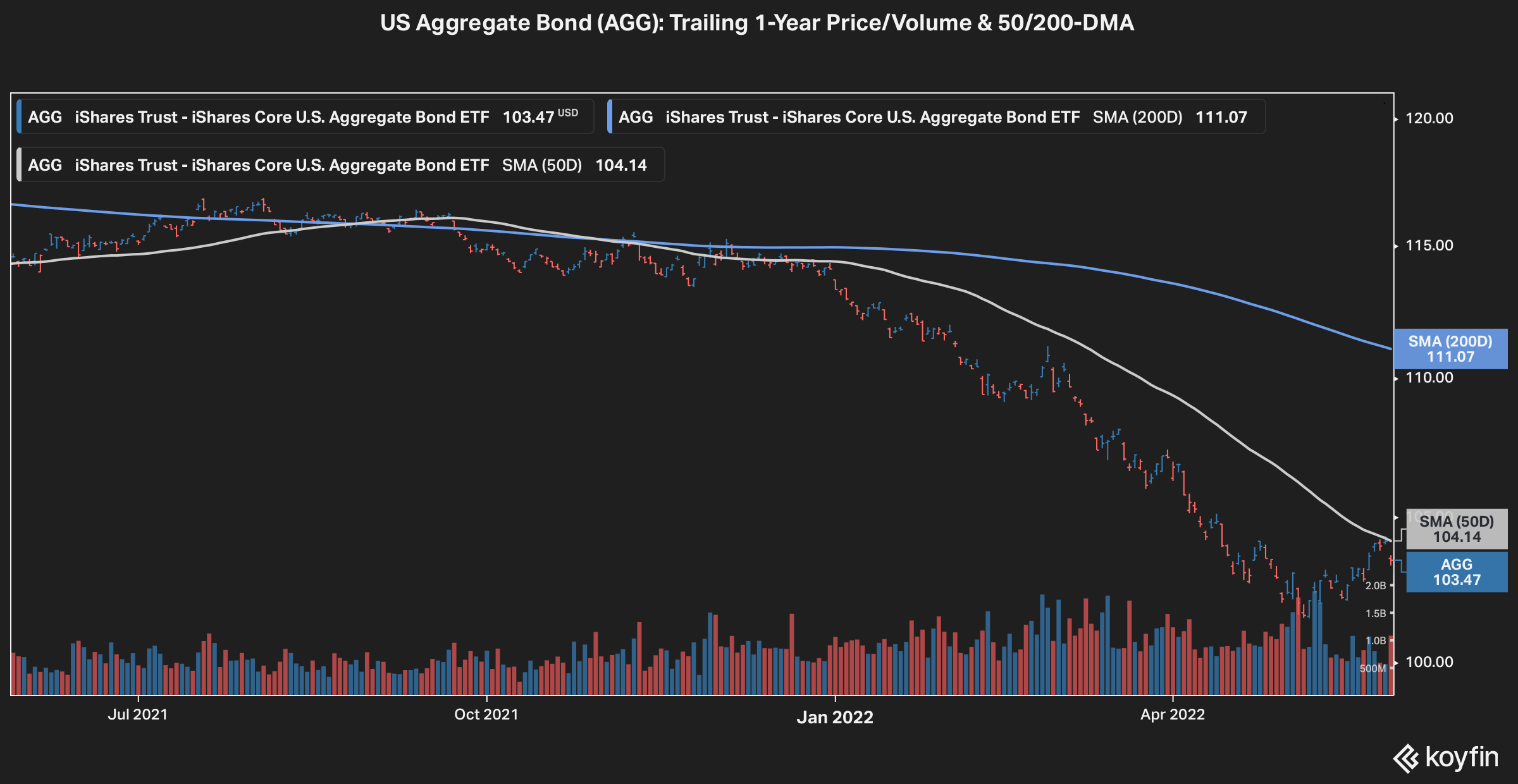

Bonds delivered mixed performance in May. US Aggregate Bond (AGG) gained 0.8% as short/intermediate rates moved lower, but UST 20+ Year (TLT) declined -2.3% in May as long-duration rates moved higher. For ‘22, AGG is down -8.7%. Spread strategies gained in May, including HY bonds and Emerging Markets debt.

Diversified Commodities (DBC) gained in May, but underlying performance was mixed. Across the four commodity sectors, only energy delivered a positive return. DBC — which is ~55% energy — gained 4.6% in May and is up 38.6% for ‘22.

US/Global Equities

Technical factors helped lift US/global equities in late May as stated above. Conceivably, weak economic data prompted a sense that the Fed may become less aggressive in its tightening cycle. Regardless, equities already were oversold and ripe for a bounce and once the move higher was triggered, short-gamma conditions and other flow-related factors amplified the move to the upside. Whether or not the gains are lasting is something we will learn soon enough.

S&P 500 (SPY) finished May with a modest gain of 0.2%. Despite an unsatisfying decline on the final day of May, SPY still rallied 6.0% over the last seven trading sessions of the month. May’s modest monthly return hides the volatility SPY displayed during the month. SPY traded in a wide range in May with a spread of ~11% based on the intraday low/high. The Volatility Index (VIX) finished the month at 26.19, down from 33.40 at the end of April.

Once again, growth-oriented shares underperformed in May. Nasdaq 100 (QQQ) declined -1.6% and is down -22.4% for ‘22. Across four simple size/style factors we follow, value delivered positive returns in May, but growth posted losses. The value/growth performance gap widened in May, but growth showed signs of life — outperforming over the last week of the month.

Across S&P 500 sectors, six were positive and five were negative in May. Energy (XLE) and Utilities (XLU) were the top performers in May with gains of 16.0% and 4.3%, respectively. Moreover, Energy and Utilities are the only two positive performers for ‘22 with YTD gains of 58.6% and 4.5%, respectively.

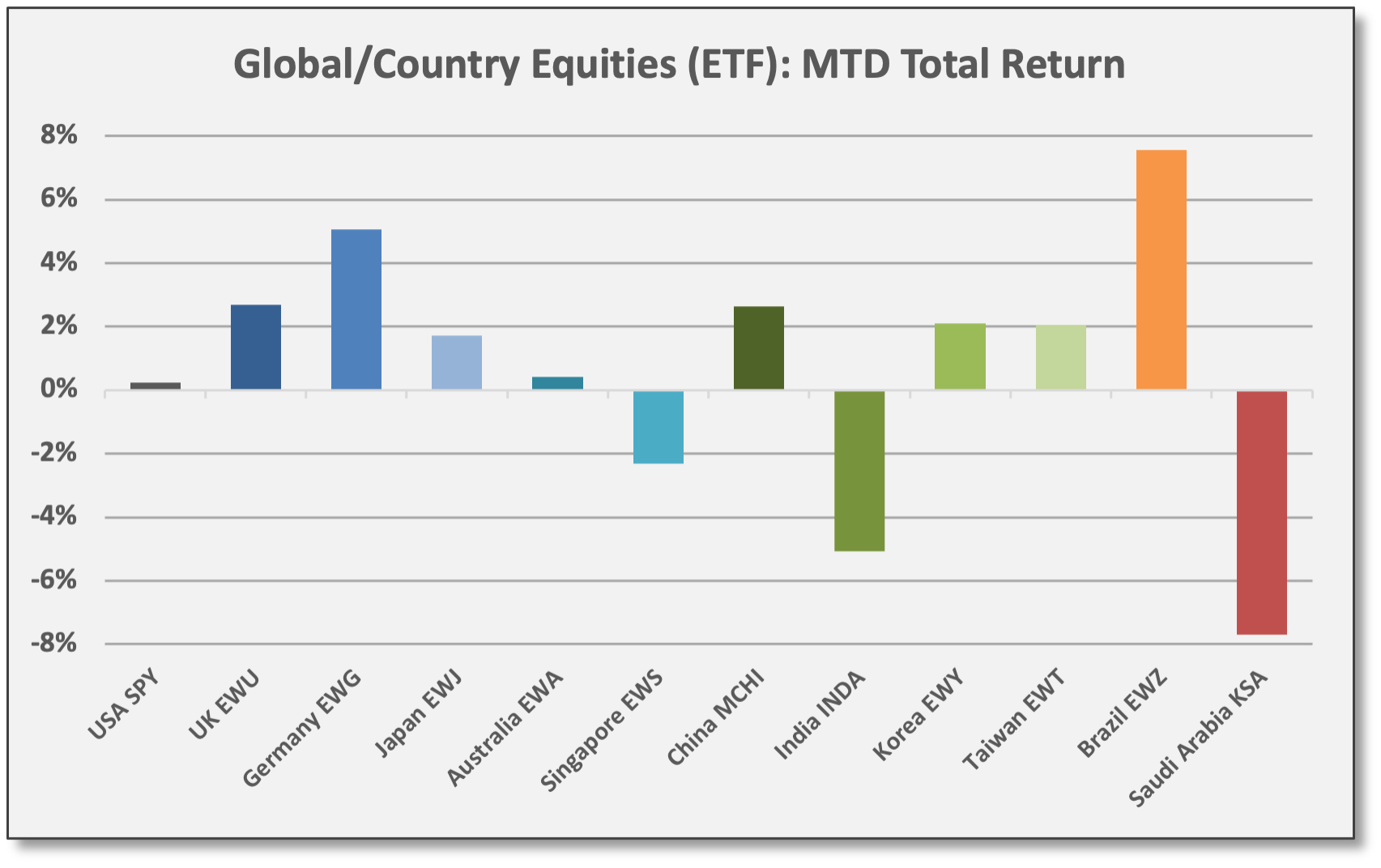

In May, Developed Markets (EFA) and Emerging Markets (EEM) gained 2.0% and 0.6%, respectively. For ‘22, EFA and EEM are down -11.0% and -12.7%, respectively. Brazil (EWZ) the top performing market in May with a gain of 7.6%; Brazil is also the top performer for ‘22 with a gain 25.6%.

Fixed Income & Credit

Bonds delivered mixed performance in May. Intermediate interest rates moved lower during the month, but rates moved higher for long-duration bonds.

US Aggregate Bond (AGG) gained 0.8% as short/intermediate rates moved lower, but UST 20+ Year (TLT) declined -2.3% in May as long-duration rates moved higher. For ‘22, AGG is down -8.7%.

Yield Curve: UST 2-year note closed May with a yield of 2.53% — down 17 bps for the month, but up 180 bps for ‘22; UST 10-year note closed May with a yield of 2.85% — down 14 bps for the month, but up 133 bps for ‘22. After briefly inverting at the start of April, the 2-10 spread finished May at +35 bps.

Spread strategies gained in May: Investment-Grade corporate bonds (LQD) gained 1.9%, but are down -12.9% for ‘22. IG spreads closed May at +141 (as of 5/30), flat for May, but down from a peak of +155 on 5/20. Corporate HY bonds (JNK) gained 1.5%, but floating-rate HY bank loans (BKLN) — with virtually zero rate duration — declined -2.0%. HY spreads closed May at +422, wider by ~30 bps for the month but down from a peak of +494 on 5/24. JPMorgan: “In High Yield, spreads are discounting a worse default outcome than has been realized at any time since 2009. That said, we think a large risk premium is justified and are not tempted to call the wides just yet.” JNK is down -7.7% for ‘22. Local-currency Emerging Markets debt (EMLC) gained 1.4% in May, but are down -9.0% for ‘22.

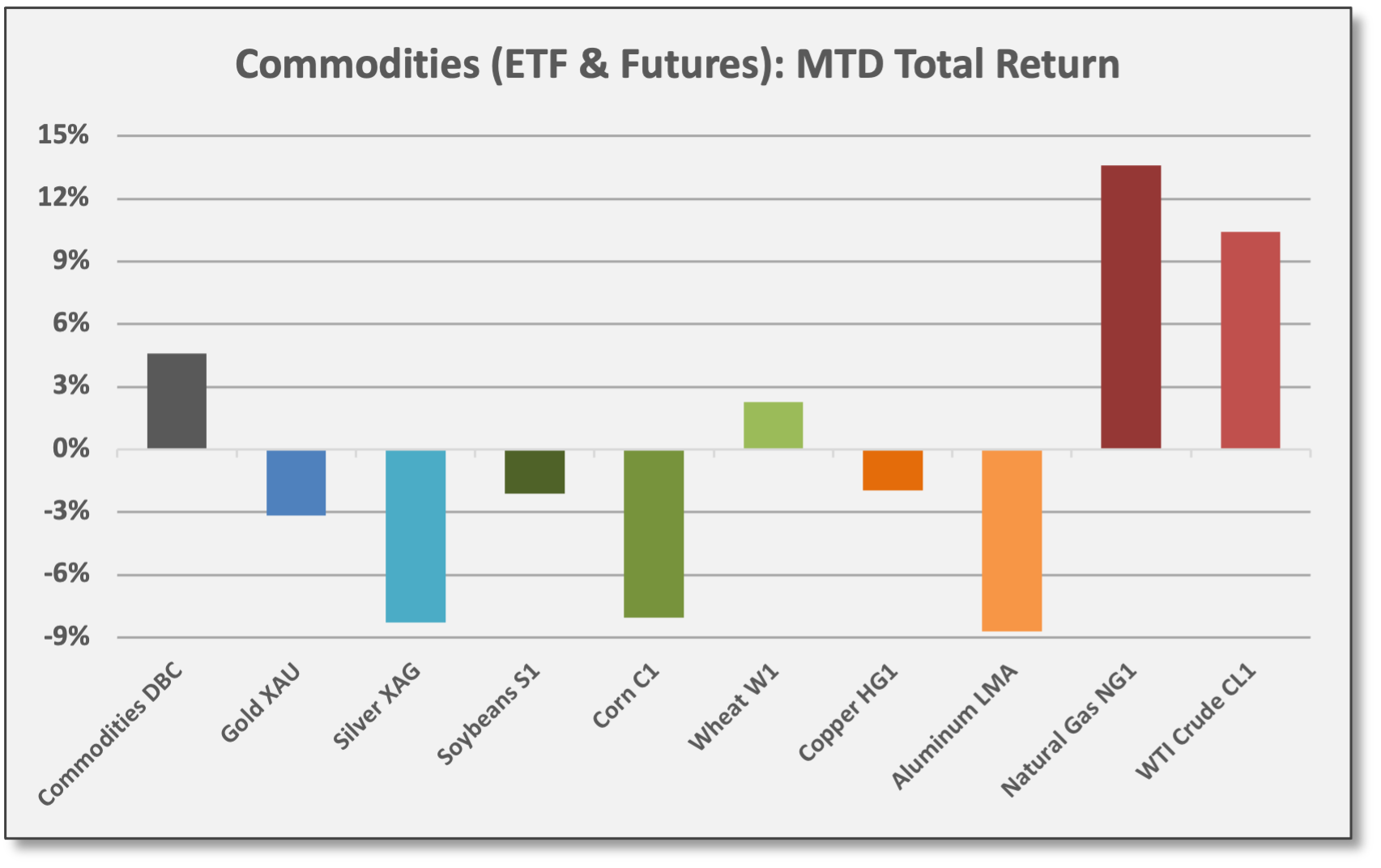

Commodities & Real Assets

Diversified Commodities (DBC) gained in May, but underlying performance was mixed. Across the four commodity sectors, only energy delivered a positive return for the month.

Diversified Commodities (DBC) gained 4.6% in May and are up 38.6% for ‘22. DBC has a ~55% weighting in energy commodities.

Energy (DBE) gained 9.3% in May. Energy is the top performer for ‘22 with a gain of 62.5%. Natural Gas (NG1) gained 13.6% for May and is up 120.6% for ‘22. WTI Crude (CL1) gained 10.4% for May and is up 53.8% for ‘22; WTI closed the month at 114.67/barrel.

Agriculture (DBA) declined -0.4% in May, but is up 11.3% for ‘22. Corn (C1) was a detractor in May with a loss of -8.1%. Wheat (W1) gained 2.3% in May and is up 41.1% in ‘22.

Precious Metals (DBP) — and primarily gold — have failed to perform as an inflation hedge this year. DBP declined -4.0% in May and is down -2.1% for ‘22. DBP is ~80% gold futures. Gold (XAU) declined -3.2% in May, but is up 0.4% for ‘22.

What Others Are Saying

Jerome Powell, Fed Chair, 5/17/22: “We have to get inflation down to 2%. We need to restore our definition of price stability — and we will do that. It will be challenging to do that. We have to slow growth to do that. Growth has to move down. That’s what has to happen for inflation to come down. We don’t have precision tools. We can’t say, ‘let’s dial [inflation] to this exact level.’ We raise interest rates. That affects financial conditions. Financial conditions affect the economy... It is not in any way a ‘surgical precision’ set of tools... There could be some pain involved to restoring price stability.” Note: Powell spoke at an event organized by The Wall Street Journal.

Lael Brainard, Fed Vice Chair, 5/23/22: “Maximum employment and stable low inflation benefit all Americans, but are particularly important for those earning less. Price stability is of greatest importance for lower-income families because they spend more than three-quarters of their paychecks on essentials like groceries, gas or bus fare, and rent — more than double the 31 percent spent by higher-income households. High inflation is our most pressing challenge. That is why we are taking strong actions that will bring inflation back down.” Note: Brainard spoke at commencement ceremonies at Johns Hopkins University.

Jefferies, 5/25/22: Given the developments in financial markets in the 3 weeks since the [FOMC] meeting, as well as some weaker economic data, there was a risk going into these Minutes that the Fed would massage the Minutes and revise them into a more dovish message. From our perspective, there was no attempt to do this. Instead, the Minutes show a strong commitment to fighting inflation and they continue to advise that interest rates are likely going to have to go into restrictive territory at some point to meet the dual mandate goals. The Fed acknowledged that financial conditions have tightened ‘by historically large amounts since the beginning of the year’ but the Minutes do not cite acute risks to the economic outlook or to financial markets as a result… The Minutes show that the Committee is still on track to raise rates 50 bps ‘at the next couple of meetings’ which translates to the June 15 and July 27 meetings at a minimum. It is plausible that this leaves the door open for a slowdown in the pace of rate hikes heading into the September meeting, but we remain very skeptical that the inflation data will justify such a move… Tightening financial market conditions and uncertainty about the outlook certainly qualify as risks, but persistently high inflation, so far above target, and the potential that inflation expectations become unhinged are greater risks. In sum, we do not see any sign that the Fed is looking to take its foot off the gas, recent comments by Atlanta Fed President Bostic notwithstanding.”

Strategas, Economic Report, 5/25/22: “The US economy looks to be slowing, but policy (which acts with a lag) is just starting to restrain still-positive growth, including in key areas like business spending.”

The Bespoke Report, 5/27/22: “There’s no way to know yet if [the late May gains for equities] marked a true turning point for the market, so it’s too early to tell if this was ‘smart money’ buying or a ‘fools rush in’ kind of rally. Big short-term bounces like this occur both at major bottoms, but also during bear-market rallies. If we do find ourselves sitting on much higher stock prices in the months ahead, what happened [during the week ending 5/27] that historians could point to? Economic data generally came in weaker than expected and there were no stellar earnings reports to point to. Inflation data does look to be stabilizing or even rolling over, and interest rates have stopped rallying for now. We did see a bit of a dovish turn in Fed commentary earlier in the week when Atlanta Fed President Bostic said it may make sense to pause in September. That dovish turn causing Fed Funds pricing to turn less hawkish is the likely culprit if we do mark a bottom, but again, it’s too early to tell.”

FSInsight, 5/28/22: “Quantitative tightening will begin at the next Fed meeting. There is still a cornucopia of risks plaguing sentiment and causing a buyer’s strike in markets. However, we are not getting the low-dispersion converging correlations that usually typify the forced liquidation and exhaustive selling that brings valuations low enough to attract buying. So, it is an environment where disciplined stock-picking could get you more alpha than usual.”

JPMorgan, Global Markets Strategy, 5/25/22: “While a slowdown seems clear, it remains an unsettled question whether we're headed for a mid-cycle slowdown or recession. Markets are increasingly pricing the latter, implying a much higher recession probability than economic data. There are currently great opportunities in segments such as Energy, small-caps, high-beta/cyclicals and Emerging Markets, many of which trade at record valuation discounts. Even for the broad market, levels may be close to bottoming given positioning, flows and sentiment, with month-end rebalances providing support over the next week and buyback executions running at 3-4x higher than trend.”

BlueBay Asset Management, 5/25/22: “The market narrative has shifted decisively towards concerns around growth and the exact timing of when a recession may hit the US. Inflation remains a major issue but there is a general feeling that inflation has peaked and will begin to moderate from here, even if it may settle at a structurally higher level when compared with pre-pandemic. Part of the reason why inflation is likely to stabilize here is the tightening in financial conditions over the last six months, which has resulted from a combination of a stronger US dollar, lower equities, wider credit spreads, and higher core yields, all of which should ultimately weigh on the demand side of the economy. This has been the playbook for most of 2022, although over the last couple of weeks momentum in the US dollar has stalled as US growth concerns have begun to weigh on US yields and challenge the level of market pricing in the front end of the US rates curve.”

This material is for informational and educational purposes only. All data has been compiled from sources believed to be reliable, but there is no guarantee of its complete accuracy.

Readers should conduct their own research or consult with their advisory team before making investment decisions.

Based on the WisdomTree Bloomberg US Dollar Bullish Fund (USDU).