Weekly Briefing: 12/19/21

Weekly Briefing: 12/19/21

Thank goodness the FOMC and options expiration are behind us...

No Weekly Briefing next Sunday as we will be on a “bye” week. The Brief will next publish on 1/2/22.

Merry Christmas & Happy Holidays

Performance & Other Observations

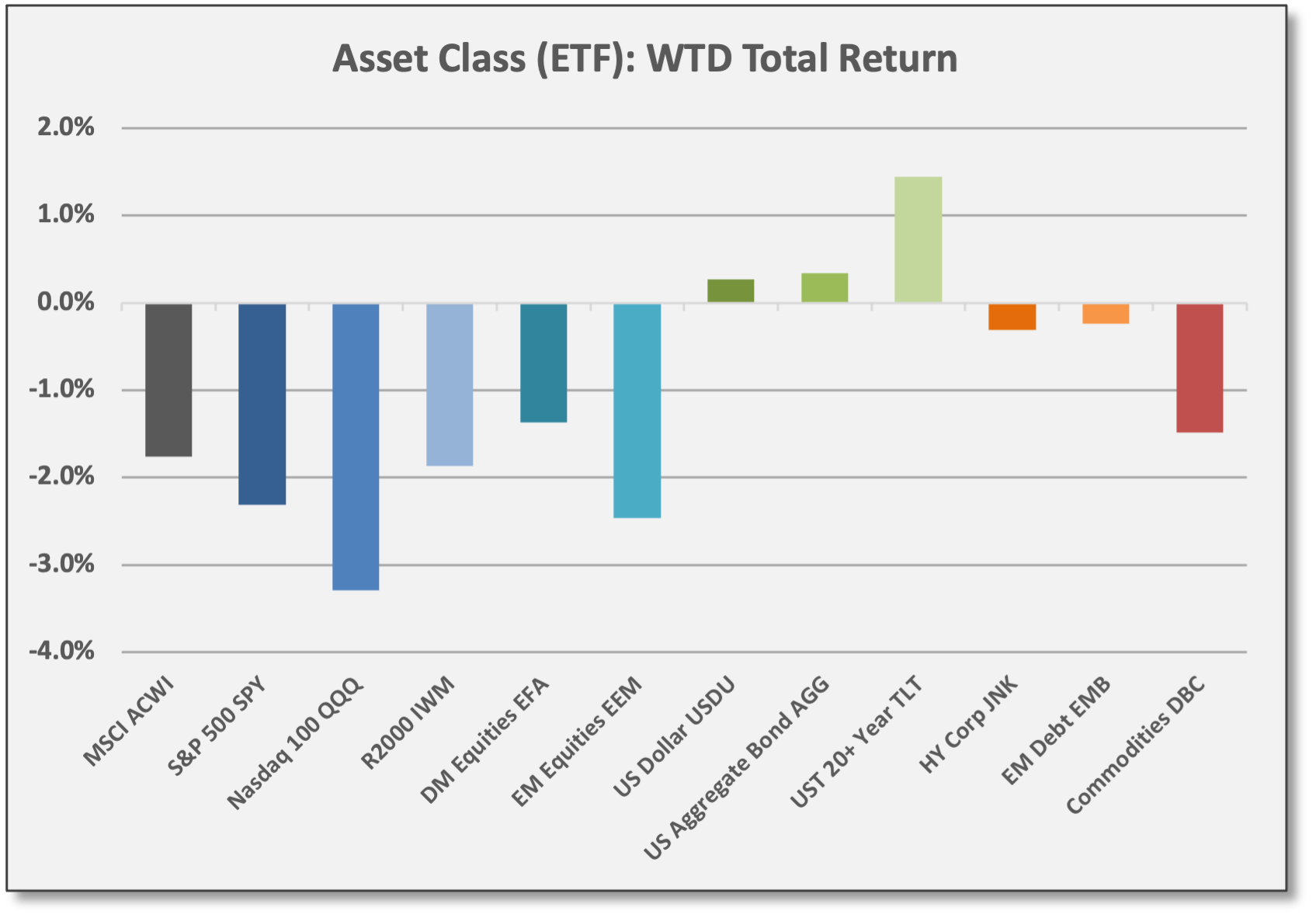

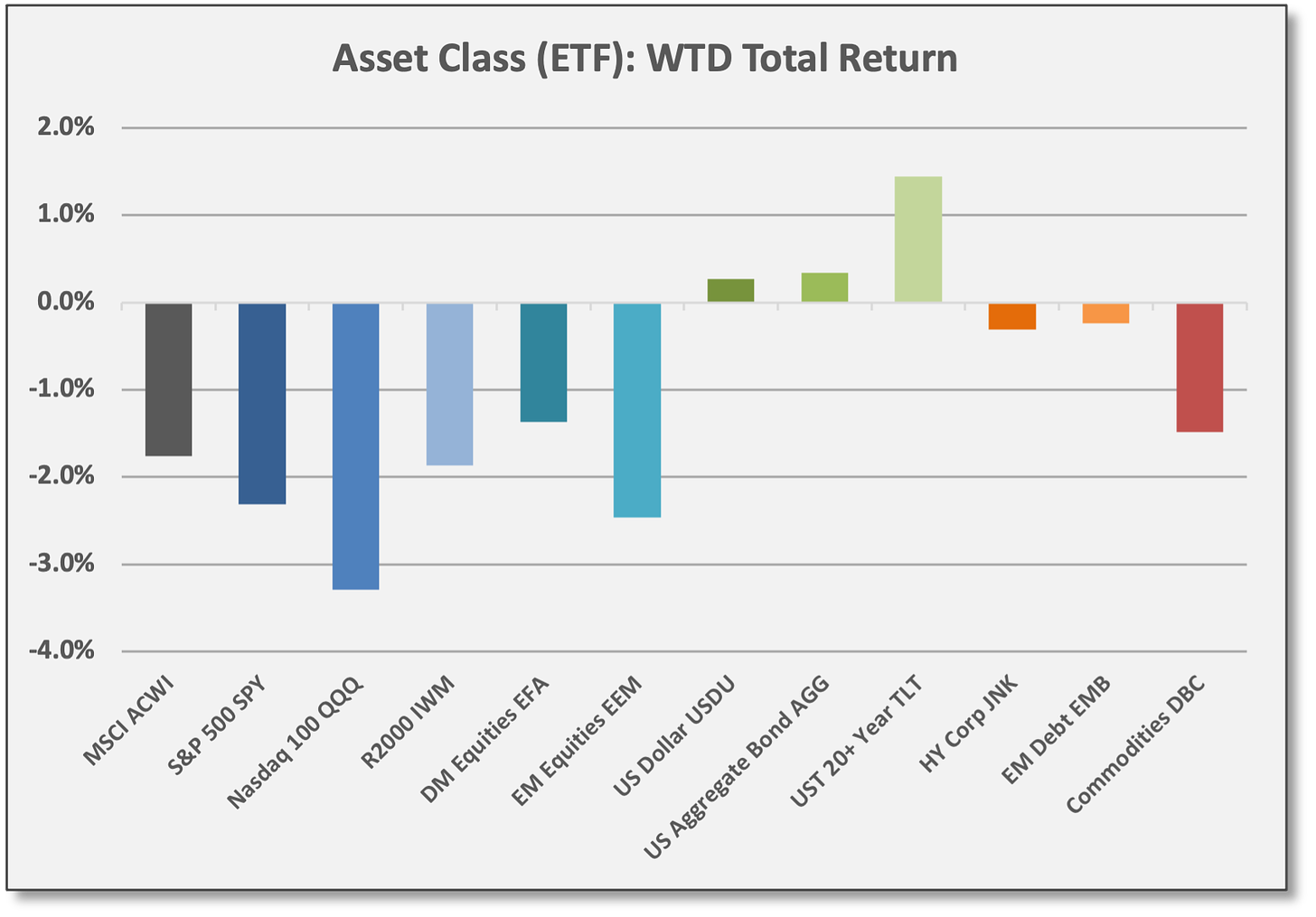

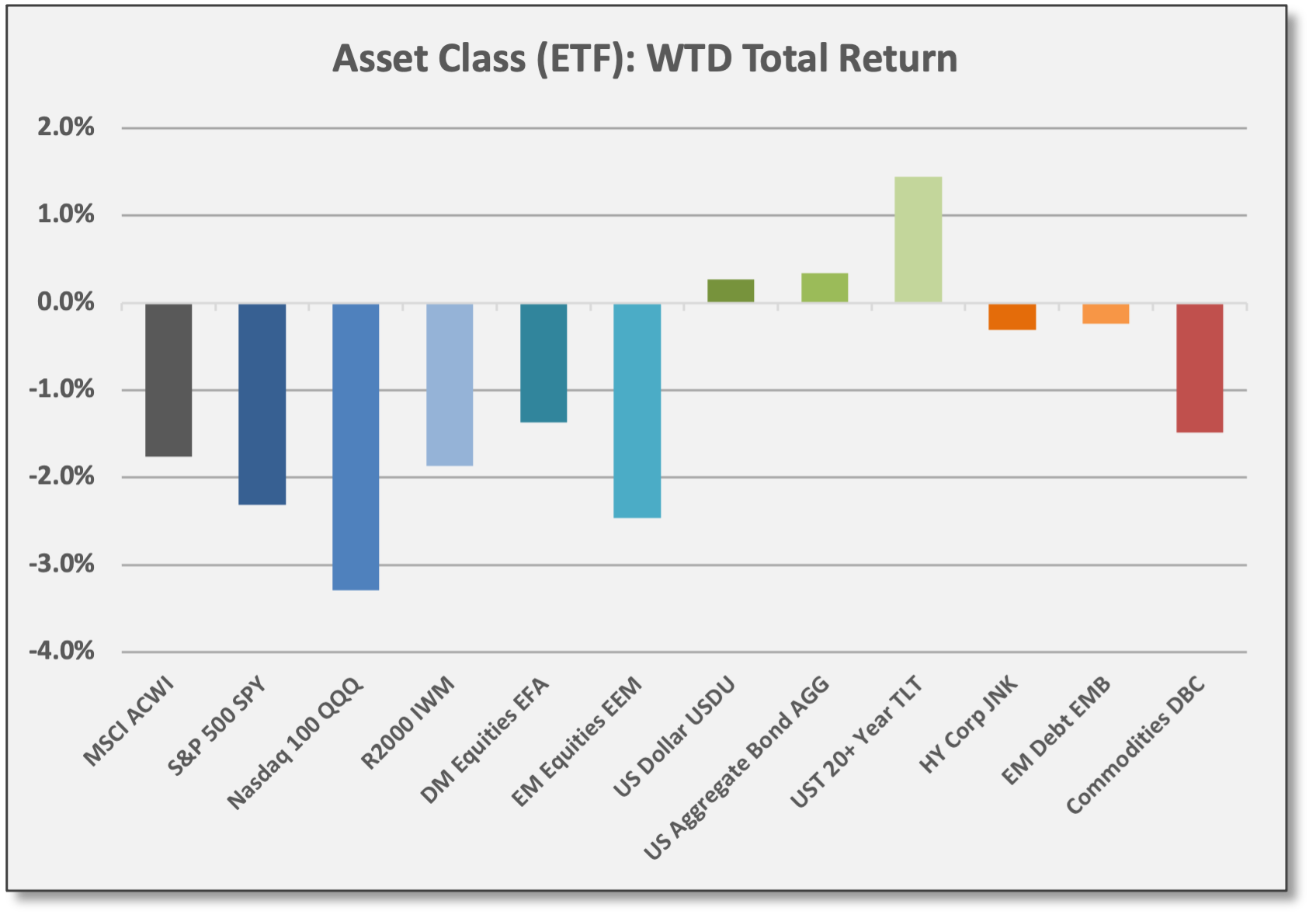

True to form, equities struggled during options expiration (OpEx) week. Defensive bonds gained. Within equities, a similar pattern was evident with defensive/yield sectors delivering gains versus declines for both cyclical/value and secular growth.

The performance divergence was stark: Notice the green-shaded bars in the two charts below.

Forced to assign a narrative to last week’s performance, we could make the obligatory reference to Fed Policy. The story goes like this: Cyclical/value equities declined on fears that higher interest rates might restrict the growth recovery and secular growth declined because higher interest rates might lead to lower valuations. In both cases, the culprit would be Fed Policy.

Indeed, the Fed confirmed it will move ahead with accelerated tapering so asset purchases will end in March 2022, paving the way for rate hikes soon after. All that sounds plausible, but there was zero news in the Fed announcement. Essentially, everything Fed Chair Powell offered has been telegraphed since early November.

Ironically, interest rates traded lower last week, so there you go… In theory, a more aggressive Fed effort to “whip inflation now” might lead to less inflation pressure in the years ahead, so that might explain rates settling lower last week.

However, discreet OpEx factors likely played a role last week, including the hedging activities of options dealers. Over short periods, these and other technical factors are capable of exerting enormous pressure on asset prices, especially when liquidity conditions are stressed or at least limited (and reportedly, liquidity depth is quite limited). As we like to say: “Never underestimate the short-term influence of non-fundamental/technical factors on asset prices.”

To summarize the risk-off week, diversified equities declined, but safe/high-quality bonds and the US dollar all gained. (Notice the green-shaded bars in the weekly performance graph.) Below the surface, there was greater performance dispersion, which is detailed further in the asset class sections referenced below.

US and non-US equities declined. S&P 500 (SPY) dropped -2.3% last week. Nasdaq 100 (QQQ) was down -3.3%.

Beta-sensitive credit declined with HY corporate bonds (JNK) and EM debt (EMB) down 20-30 basis points.

High-quality bonds and the US dollar gained. Long-duration US Treasury bonds (TLT) gained 1.4% as interest rates moved lower.

Sources: CCM, Koyfin

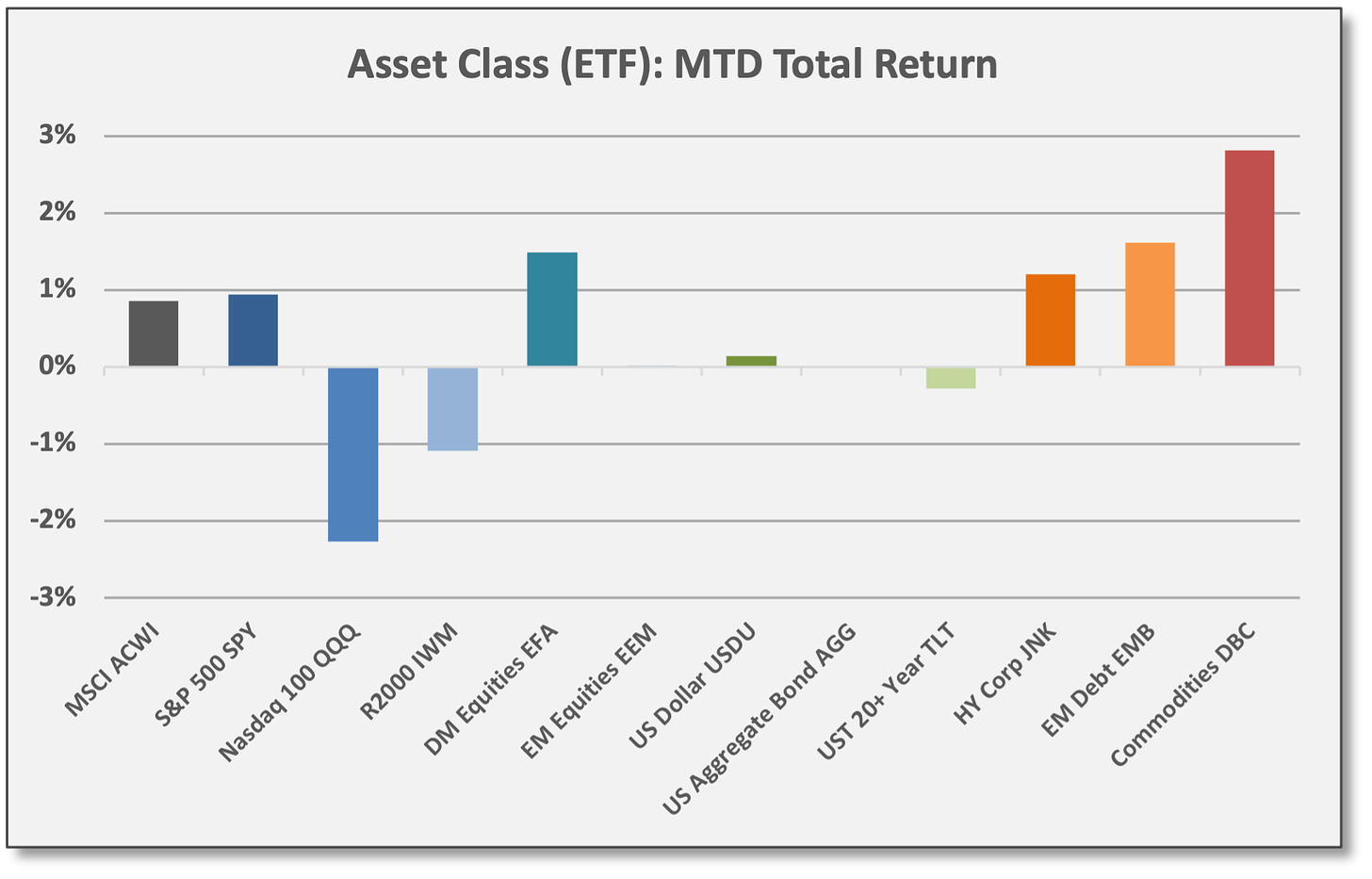

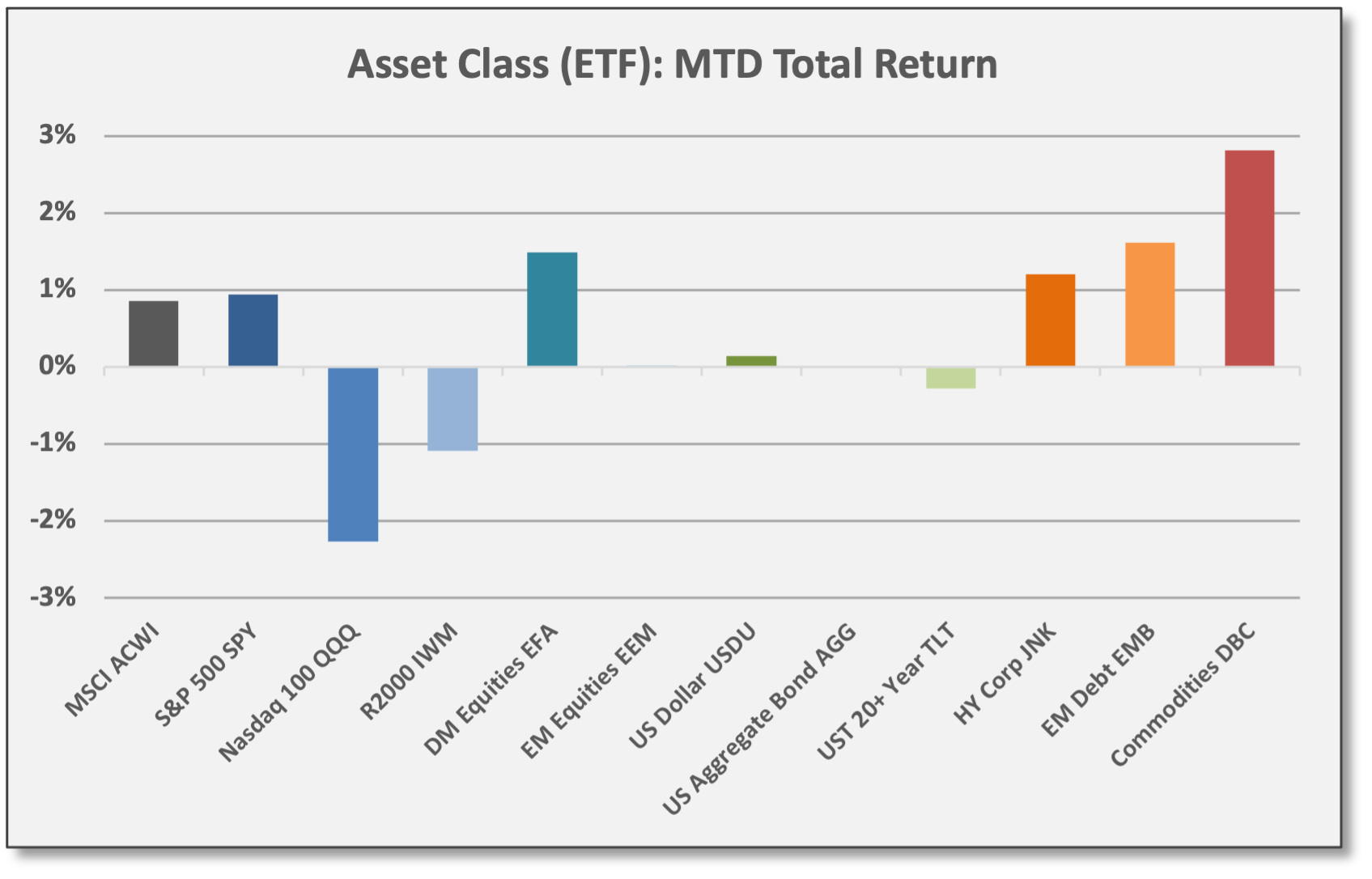

For December: Broadly diversified US equities are modestly positive, so far, but proxies for cyclical/value and secular growth are mostly flat/down. Seasonal trends point to gains for the S&P 500 into year-end and with options expiration behind us, this might unfold.

SPY is up 1.0% for December, but Nasdaq 100 (QQQ) and Russell 2000 (IWM) are down -2.3% and -1.1%, respectively.

Developed Markets (EFA) are the exception to the rule. Viewed as a value/cyclical proxy due to sector/industry exposures, EFA is up 1.5%.

Sources: CCM, Koyfin

Sources: CCM, Koyfin

In 2022, the Weekly Briefing will be available ONLY to paid subscribers. To ensure continued full access to Coffee & Capital Markets, please consider joining our research-driven community as a paid subscriber.

Economic Data & Trends

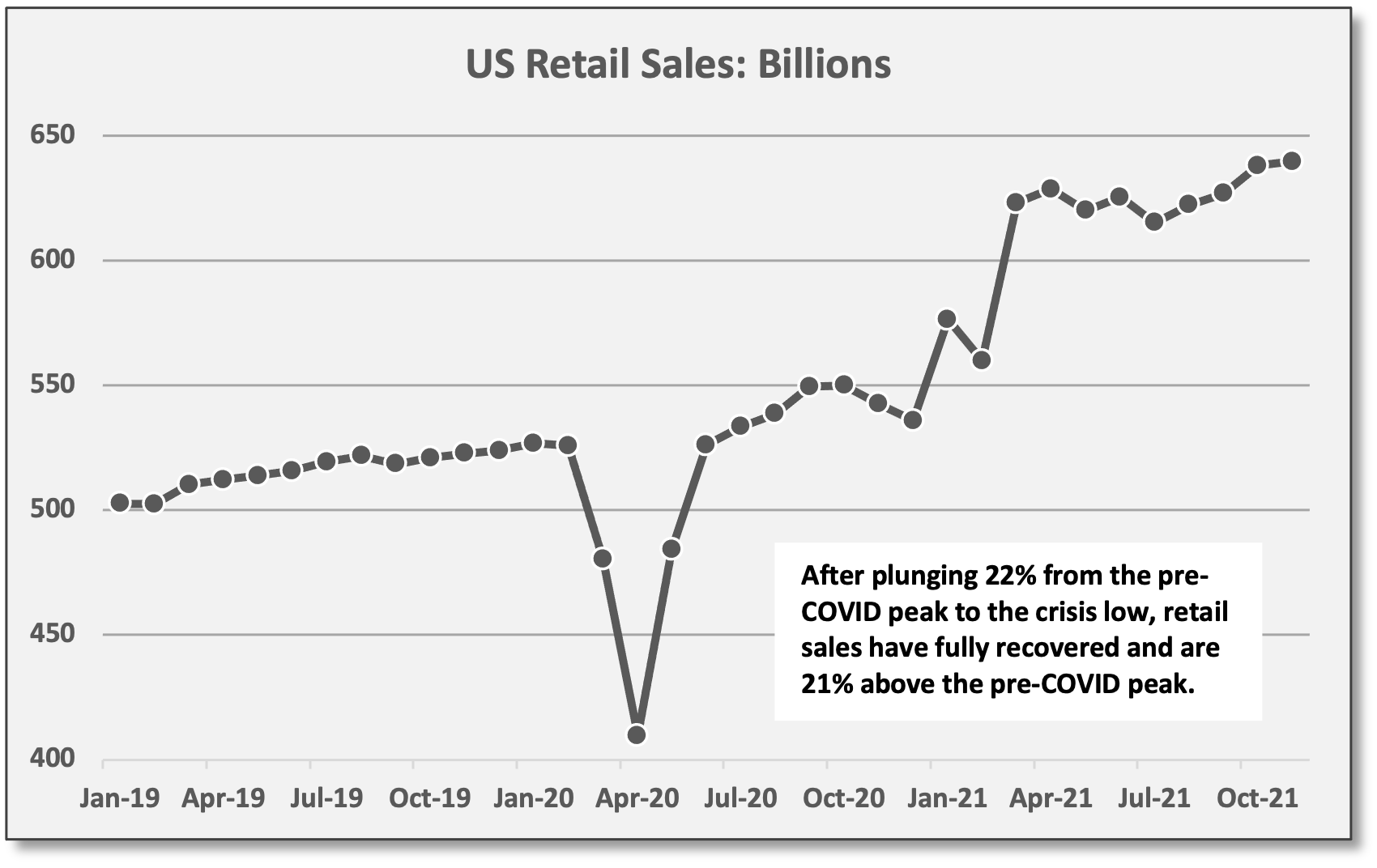

Retail Sales “disappointed” for November, increasing by 0.3%, but missing estimates. Keep in mind, monthly data ebbs and flows. Sales were up at a slower pace versus the huge October gain of 1.8% when alert shoppers pulled forward holiday spending (probably concerned about supply shortages and delivery delays) . Top categories in November were (1) food & beverage stores, (2) gas stations, and (3) restaurants & bars with the latter showing the best YTD sales growth at 44.0% as the reopening and consumer “movement” has progressed.

Over the last year, retail sales are up 18.2%, but that’s an unsustainable pace boosted by federal stimulus payments. Sales surged higher last March, so the “base effects” will take hold in March 2022, making comparisons more difficult. Thus, one-year growth rates will probably return to the low/mid-single digits. Compared to pre-COVID levels, sales are higher by 21.4%.

With lower retail sales, Jefferies reduced its Q4 GDP estimate to 7.9%. Jefferies: “After a very strong start to Q4, retail sales lost momentum in November… One notable area of weakness was electronics/appliances, which suggests that people either pulled forward those large ticket purchases to October, or they just couldn't find product to buy… Q4 GDP estimates will come down after today's data. We were assuming 6% growth in real consumption, which is now on track for 4.5% growth. This downgrade shaves 1.1% from Q4 GDP, which we previously estimated at 9%. Needless to say, Omicron creates further downside for December, and even more so for Q1, however we remain constructive on the consumer in 2022.”

Meanwhile, GDPNow from the Atlanta Fed is estimating 7.2% growth in Q4.

Industrial Production: Supply response should help alleviate price pressures. Industrial Production rose 0.5% in November, just missing estimates, but there were “very constructive details” from inside the report in the words of Bespoke Investment Group. Manufacturing was strong, especially automotive production/parts — a possible indicator that supply-chain pressures related to semiconductors are easing. Indeed, we have been hearing reports about semiconductor production ramping up and perhaps those crucial inputs are finally flowing to other industrial manufacturing sectors.

“…barring a renewed surge in consumer demand, the outlook is more likely to see a return to normal prices…” Bespoke, The Closer, 12/16/21

Bespoke: “[The IP report] suggested supply responses were under way which may start to alleviate extremely high demand for consumer durables which has created unusually high core goods inflation… barring a renewed surge in consumer demand, the outlook is more likely to see a return to normal prices than a continued unprecedented surge from durables.”

Fed sees inflationary GROWTH. Earlier this year, markets panicked over the possibility of stagflation. CPI was surging and virus concerns collided with fears of a Fed Policy mistake. Economic activity did pause in Q3 during the delta variant wave, but spending activity was mostly just delayed. Omicron might have a similar “delayed spending” effect — especially in the Northeast where the policy response could be the most pronounced.

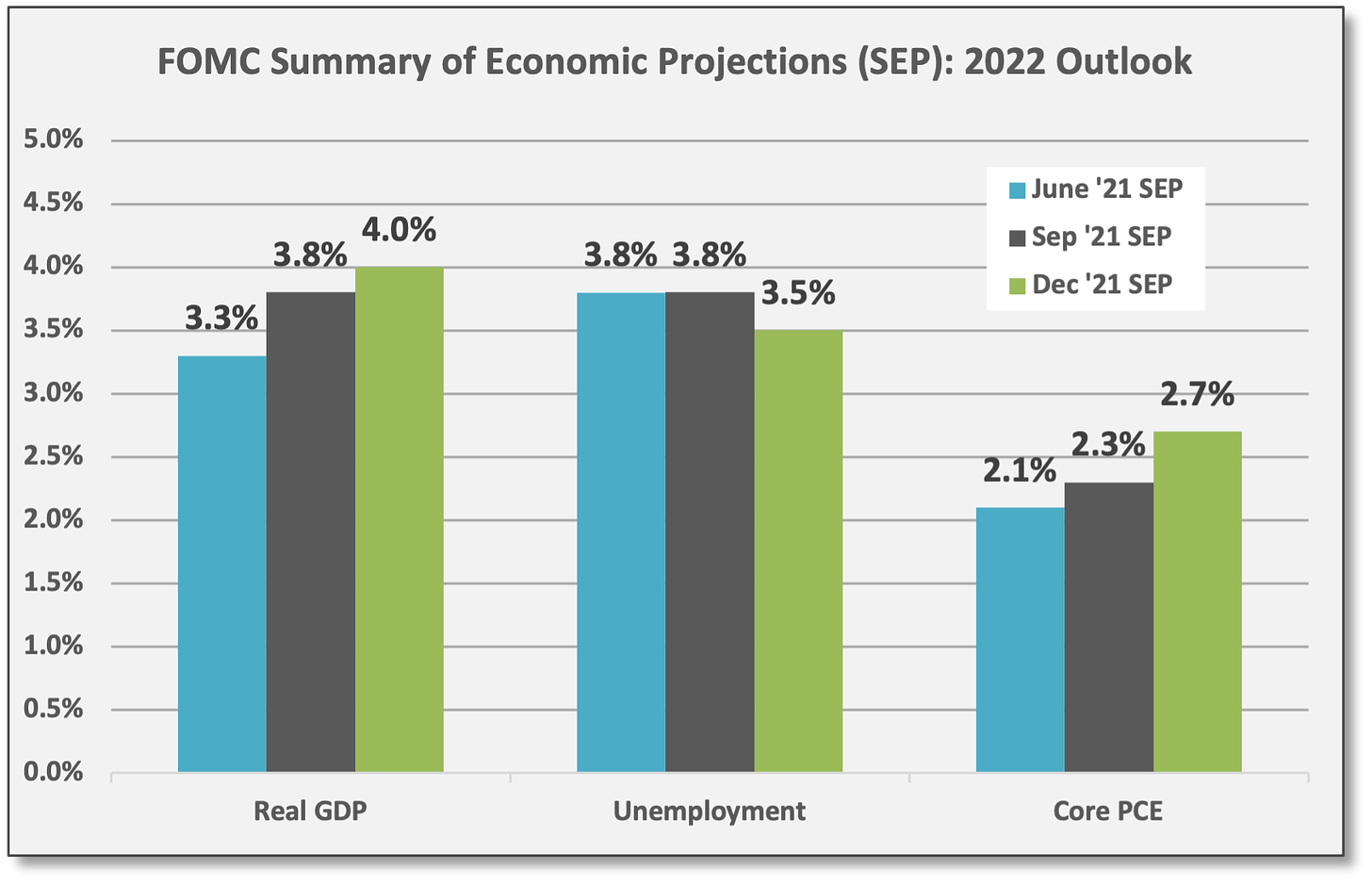

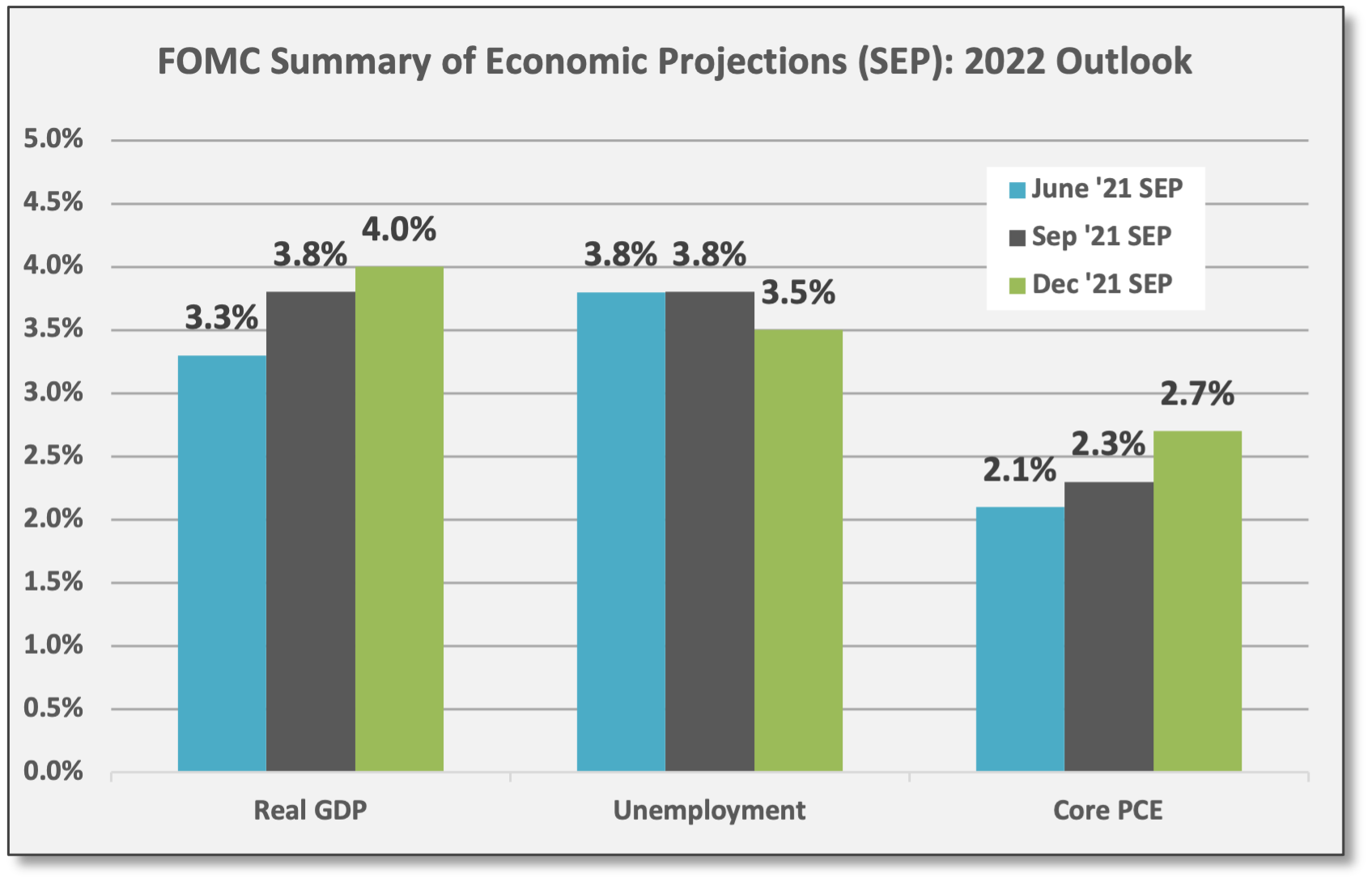

However, the Fed’s latest Summary of Economic Projections (SEP) shows a confident path for economic expansion that should drive further job gains. FOMC raised its median forecast for GDP growth and core inflation for 2022 with both metrics predicted to show above-trend growth. Unemployment is seen falling to a level below the Fed’s threshold of long-run full employment (4.0%).

GDP growth forecast increased to 4.0%

Core PCE inflation forecast increased to 2.7%

Unemployment rate forecast to fall to 3.5%

Sources: CCM, US Federal Reserve Bank

Fed forecasting tends to be conservative, so the fact the Fed is upgrading its growth outlook is a positive indicator. In short, economic activity in 2022 should remain well above trend (although the month-to-month ride could be bumpy until policymakers and business leaders learn to better cope with an increasingly low-severity virus and control their collective impulses to impose movement restrictions).

FOMC forecasted GDP growth of 4.0% for 2022 is roughly 2x the recent trend rate.

In fact, the SEP shows an expected long-term GDP growth rate of just 1.8% (median) with a “central tendency” range of 1.8% to 2.0%.1 Since 2009, the post-GFC era, US GDP growth has averaged 2.1% per quarter (annualized). Thus, the FOMC forecasted growth of 4.0% for 2022 is roughly 2x the recent trend rate.

Monetary/Fiscal Policy

As expected, the Fed announced it will move ahead with accelerated tapering — reducing its monthly asset purchases at a faster rate. The revised tapering plan was originally outlined at the November meeting and telegraphed repeatedly by Powell and FOMC colleagues in recent weeks. The Fed also dropped its reference to inflation being “transitory.”

However, any reports that the Fed is aggressively “hawkish” seem overstated in our view.

Bespoke: “To be sure, this was not a dramatically hawkish announcement; the Fed still wants maximum employment, still doesn’t feel forced to hike immediately, and still doesn’t see inflation spiraling out of control.”

Real interest rates remain negative so Fed Policy remains accommodative and is nowhere near restrictive.

Frankly, we see the Fed decision as reassuring in the sense that the Fed sees persistent strength in economic growth and employment trends. In fact, the FOMC upgraded its 2022 forecasts for both. Thus, the Fed believes there is no need for COVID-related “emergency measures” to continue. At the same time, real interest rates remain negative so Fed Policy remains accommodative and is nowhere near restrictive.

As it stands, the Fed’s quantitative easing program should end in March 2022.

By raising its core inflation forecast from 2.3% to 2.7%, the FOMC made a sharp upward revision. The Fed’s inflation forecast is based on Core PCE2 which strips out food and energy costs just like Core CPI.

Core PCE was up 4.1% over the last year as of October. For comparison, Core CPI was up 4.6% over that same period (and 4.9% as of November).

Jefferies: “There are still downside risks to growth posed by COVID and other factors, but the tilt of the [FOMC] statement shows that the Committee has shifted from a stance of propping up the recovery at all costs, to one where balancing inflation and inflation expectations is going to be a much bigger factor.”

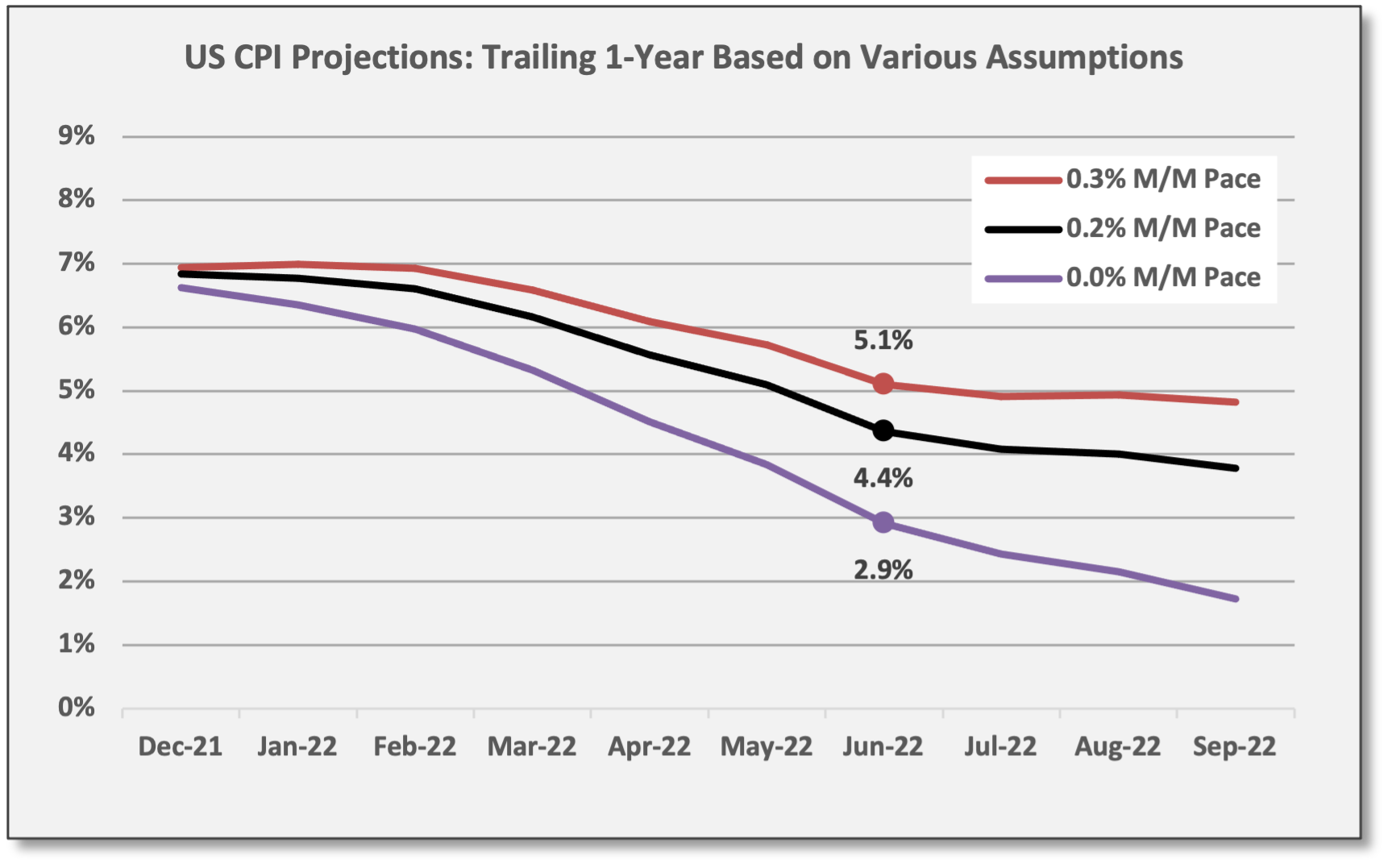

What to expect assuming inflation grinds lower in the months ahead. With semiconductor production ramping up and supply-chain pressures gradually easing, inflation will almost certainly trend lower in 2022 compared to current levels — even if overall prices remain elevated versus pre-COVID conditions.

If CPI immediately slowed to a month-to-month increase of 0.2% and sustained that pace going forward, then trailing one-year CPI would still be 4.4% in June ‘22.

As a thought exercise, Jefferies projected where trailing one-year CPI would be in the months ahead based on various assumptions. We replicated that modeling to highlight where inflation data might be when the FOMC meets to ponder rate hikes in March and June.

For context, monthly CPI increases have been 0.9%, 0.5%, 0.3%, 0.4%, 0.9%, and 0.8% over the last six months — an annualized pace of 7.6%.

If CPI immediately slowed to a month-to-month increase of 0.2% — or 2.4% annualized — and sustained that pace going forward, then trailing one-year CPI would still be 6.2% in March ‘22 and 4.4% in June ‘22.

More dramatically, if CPI dropped all the way to zero next month and sustained that pace going forward, one-year CPI would be 5.3% and 2.9% next March and June, respectively.

Obviously, if inflation trends come down more slowly, trailing one-year levels will remain higher than illustrated.

Hence, investors need to brace for elevated inflation prints even if price trends turn lower. Granted, our illustration focused on headline CPI rather than Core CPI or Core PCE (excluding food and energy), which both tend to run lower.

As an aside, the Fed’s 2.7% core inflation estimate for 2022 implies an average monthly price increase of 0.22%.

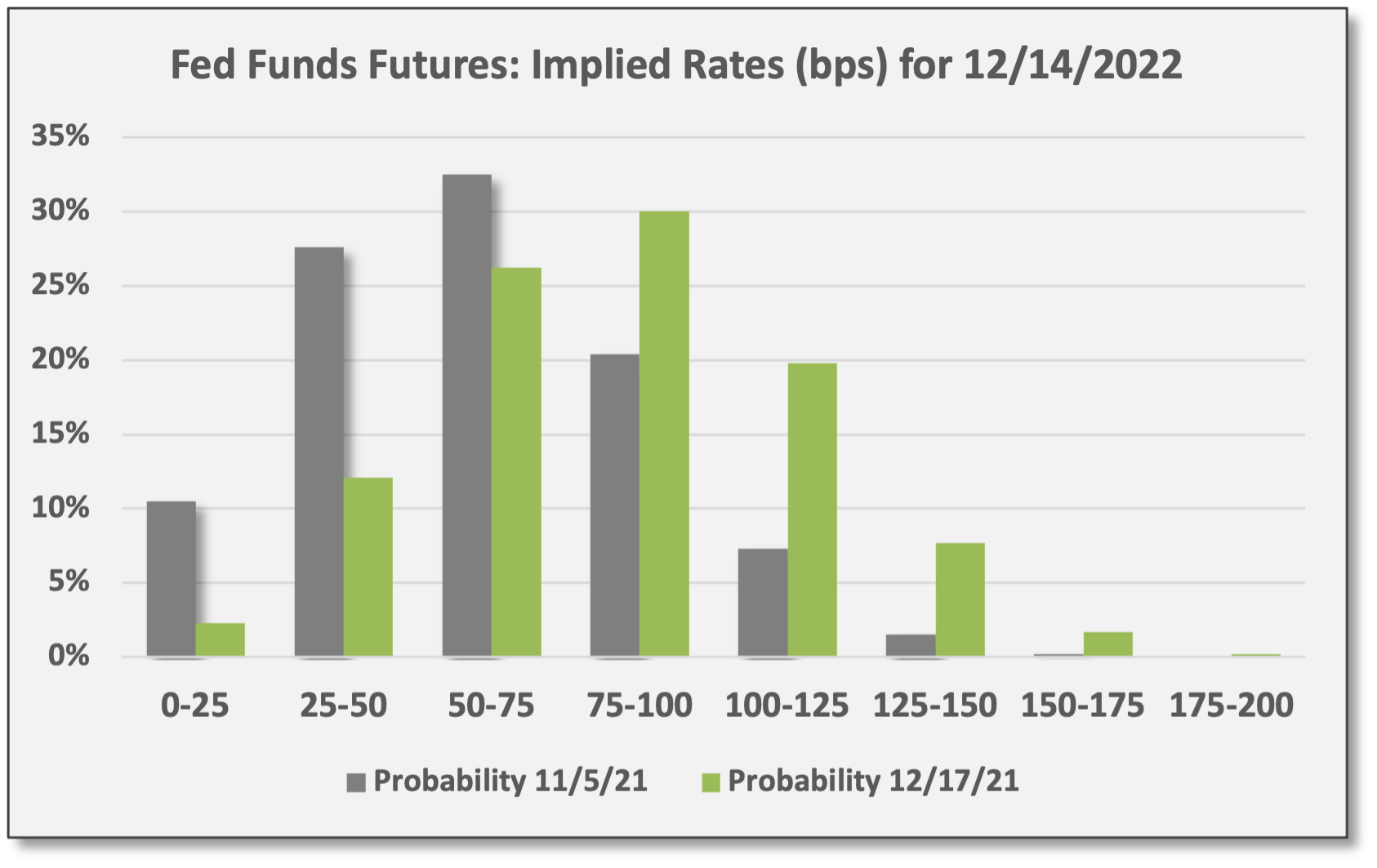

The more relevant questions surround when the Fed might begin boosting short-term policy rates and by how much. Powell emphasized that rate hikes will be considered separately from the tapering program. There is no set timetable for when hikes might commence, but Powell assured markets that hikes will only come after tapering is complete. That circles May 2022 as the earliest possible launch date.3

Sure enough, market-based pricing expects the first rate hike in May with a total of three hikes by year-end 2022. Three hikes next year seems about right.

Fed Funds futures currently show a ~60% probability of a May 2022 hike.

In addition, futures are pricing a ~60% probability of three or more hikes by year-end 2022 — up from a ~30% probability after the November FOMC meeting. Essentially, markets now see the Fed’s effort to address inflation as more substantial compared to a month ago.

Sources: CCM, CME Fed Watch Tool

From what we gather, the May launch date might be aggressive. A more patient Fed might begin the hiking process at the June FOMC meeting, followed by two more hikes in September and December, but these are subtle timing differences.

Three Fed hikes next year would put target policy rates at 0.75% to 1.00%. If core inflation drops to 2.7% as the Fed predicts — Fed Policy will remain firmly accommodative with negative real rates.

Keep in mind that Q4 economic growth looks to be quite strong and that data will be reported early next year, so that could give greater momentum and market acceptance to an earlier move by the Fed. All that said, three Fed hikes next year would put target policy rates at 0.75% to 1.00%. If core inflation drops to 2.7% as the Fed predicts — Fed Policy will remain firmly accommodative based on negative real rates.

Last week, the Bank of England hiked rates from zero to 0.25%.

Fiscal Policy: No Big Spending Before the Mid-Terms. With limited support for its green spending initiatives and other social programs, particularly among moderate Democrats, the Biden Administration admitted its Build Back Better plan will be delayed, perhaps indefinitely. With high inflation becoming an increasingly difficult political hurdle for Democrats, the plan will be tabled for now, especially with analysis showing the plan could add to existing inflation pressures.

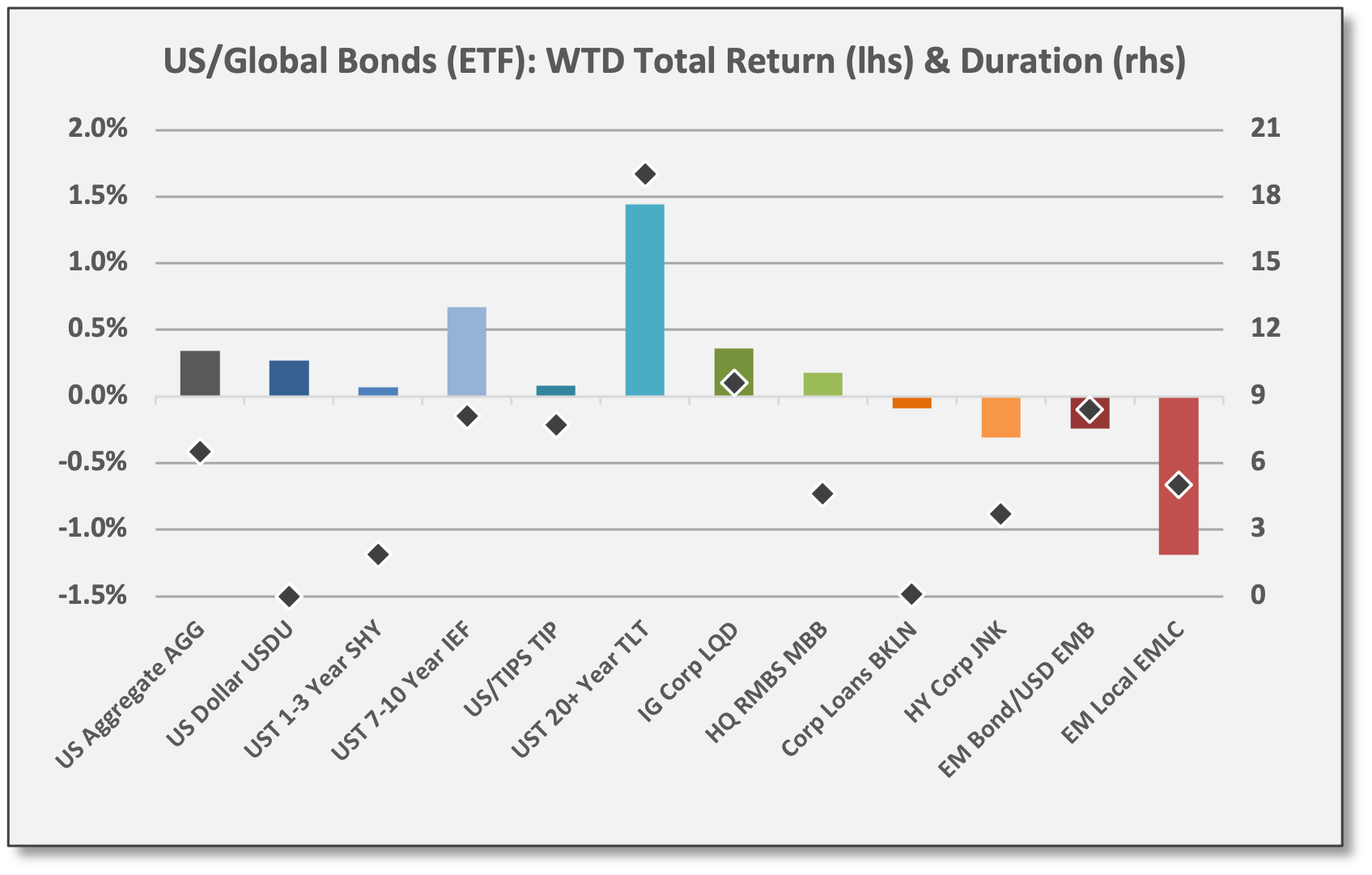

Fixed Income, Rates & Credit

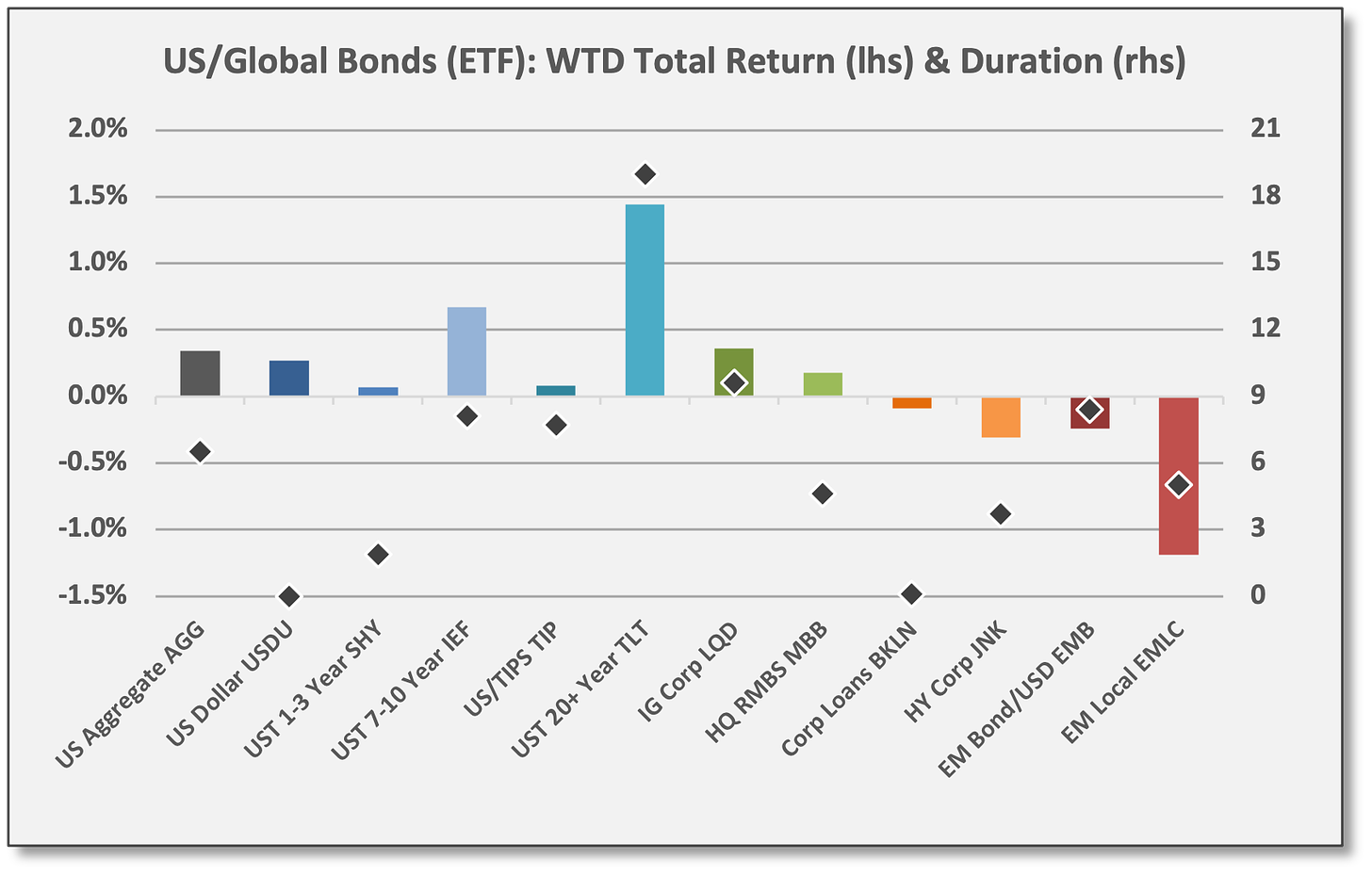

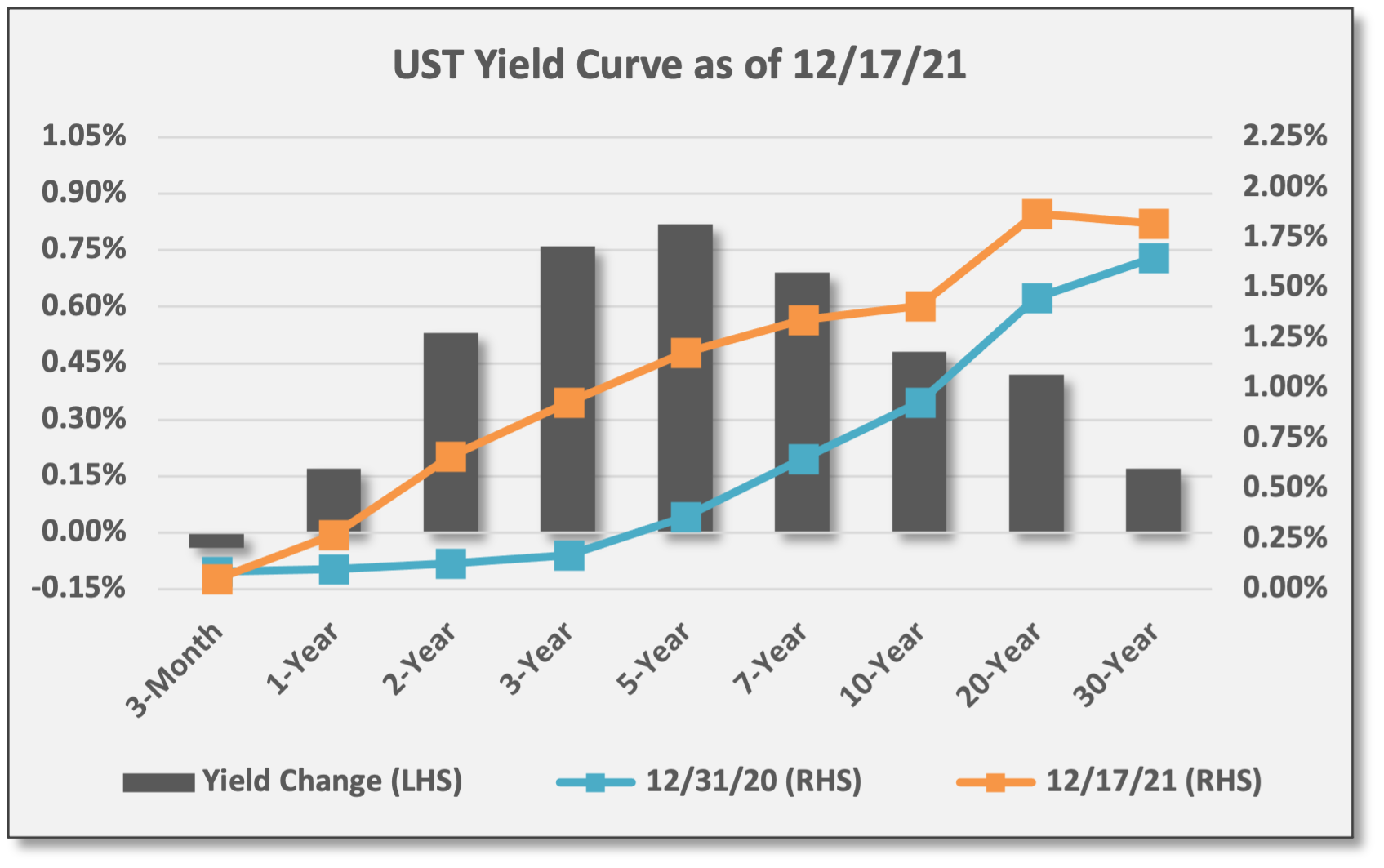

Rates moved lower and high-quality assets gained last week. The benchmark UST 10-year note closed at a yield of 1.41%; the yield was down seven basis points for the week, but 10-year yields are up 48 basis points for 2022.

US Aggregate Bond (AGG) gained 0.3%. All sectors contributed positively — USTs, IG corporates, and MBS.

UST 20+ Year (TLT) was the top performer last week with a gain of 1.4%. The yield for the 30-year bond dropped six basis points to 1.82%. Long bond rates are up just 17 basis points for 2022.

Credit spread strategies declined last week. HY corporates showed their equity beta and spreads inched wider. EM debt reversed lower after posting gains for most of the month — suffering in part due to a stronger US dollar.

Sources: CCM, Koyfin

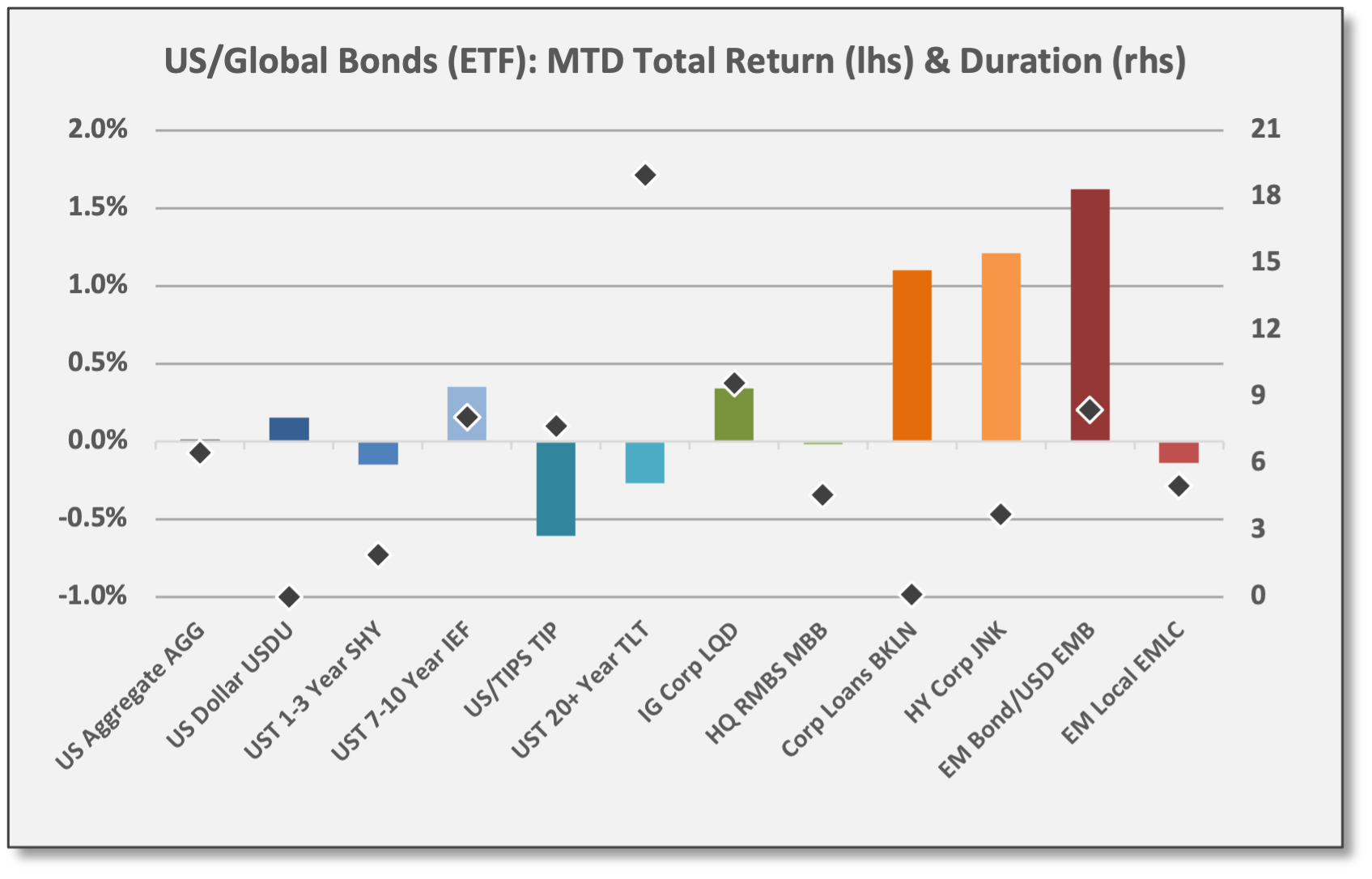

For December: Growth and beta-sensitive credit sectors are still outperforming.

HY corporate bonds (JNK) and floating-rate bank loans (BKLN) are delivering gains of 1.1% and 1.2% so far this month, respectively.

Emerging Markets (EMB) — USD-denominated — are the top performer with a gain of 1.6%. USD-based EM bonds have less foreign currency risk.

Sources: CCM, Koyfin

Sources: CCM, Koyfin

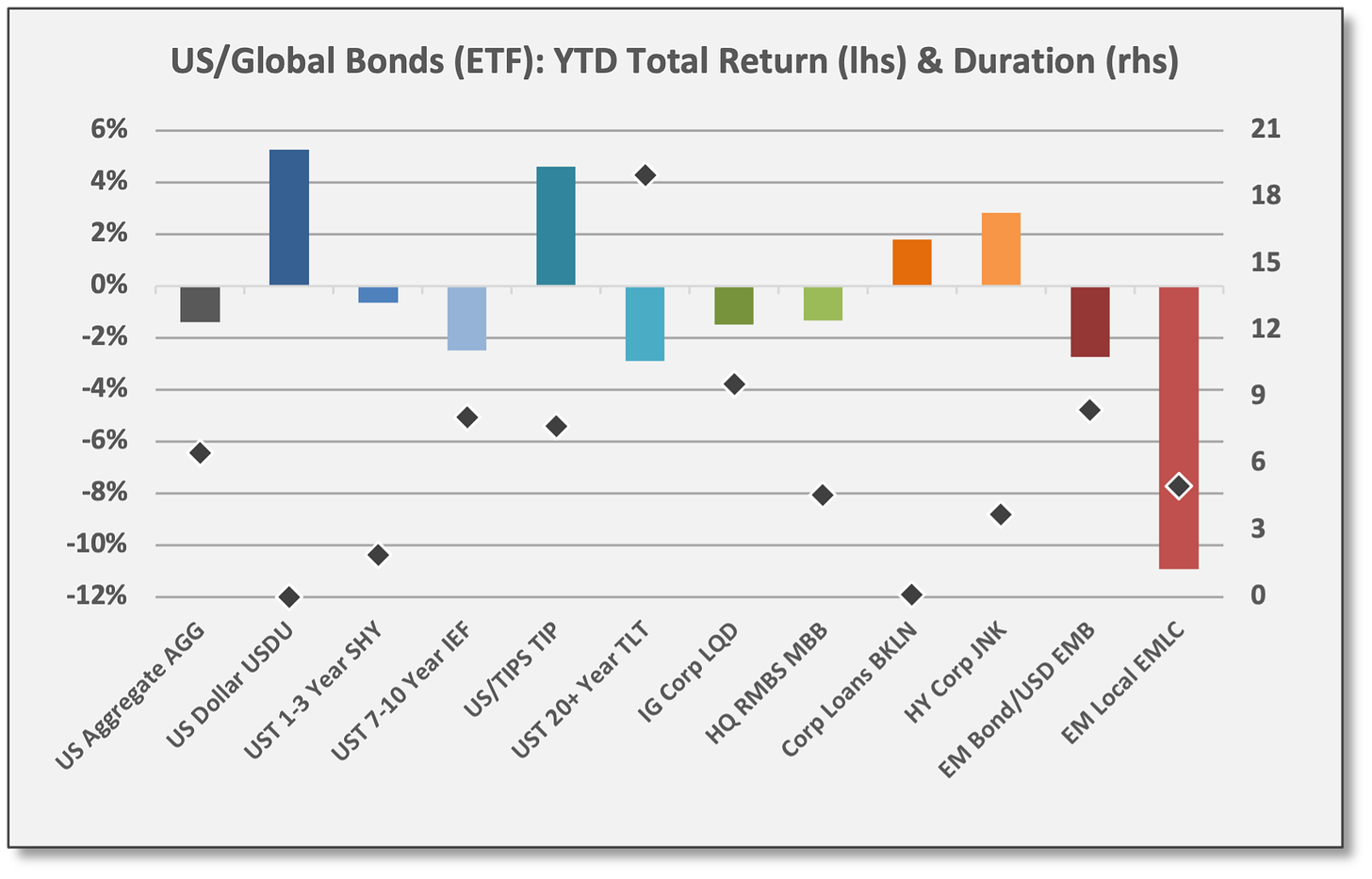

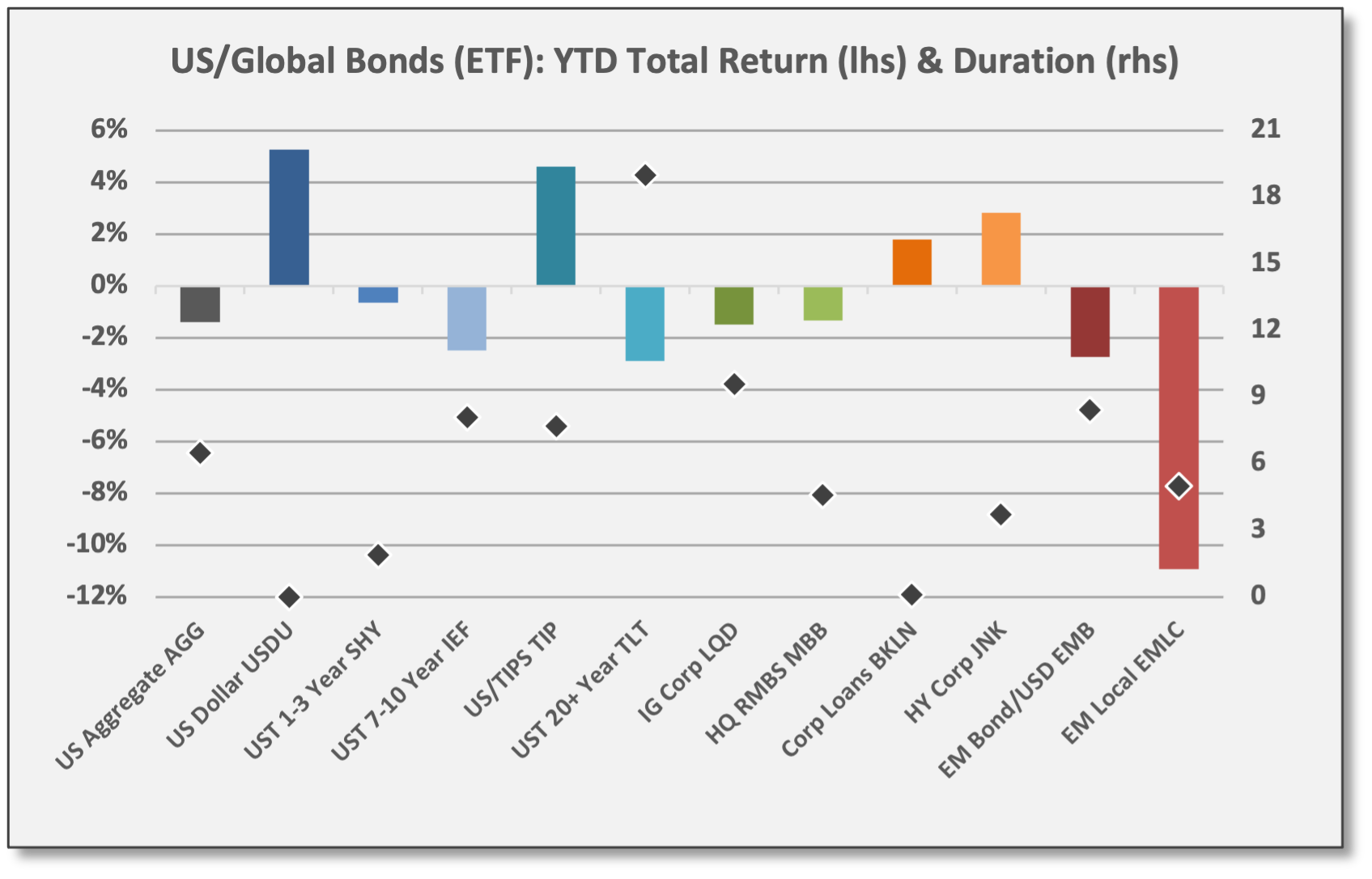

For 2022, the yield curve has flattened, but remains upward sloping, consistent with economic expansions. The 2-10 spread is virtually unchanged (narrowing from +80 basis points to +75) this year, but the 2-30 spread has narrowed from +152 to +116. For all the fear about higher interest rates, moves have been limited this year.

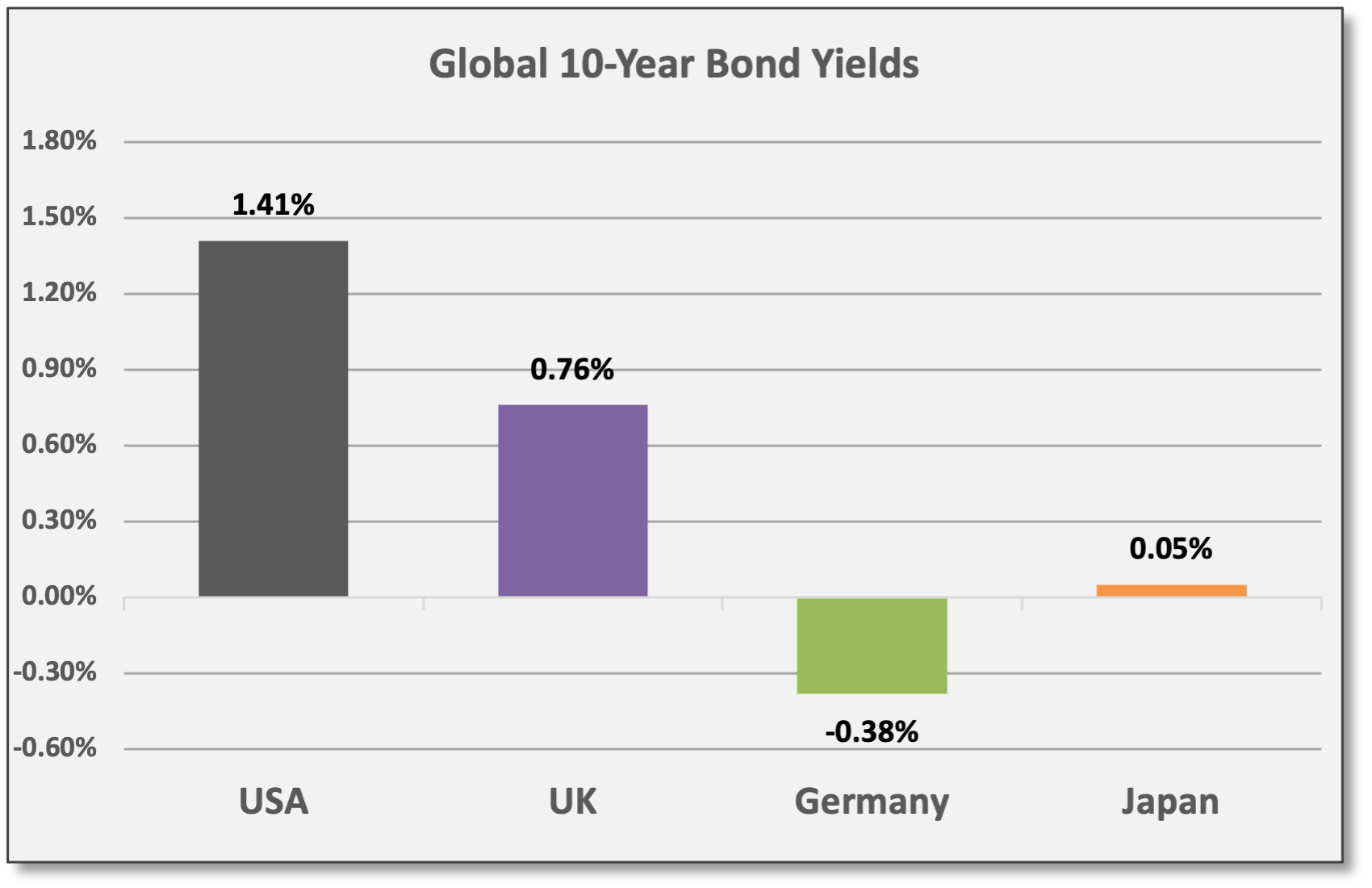

USTs continue to show a large spread advantage versus major foreign bond markets.

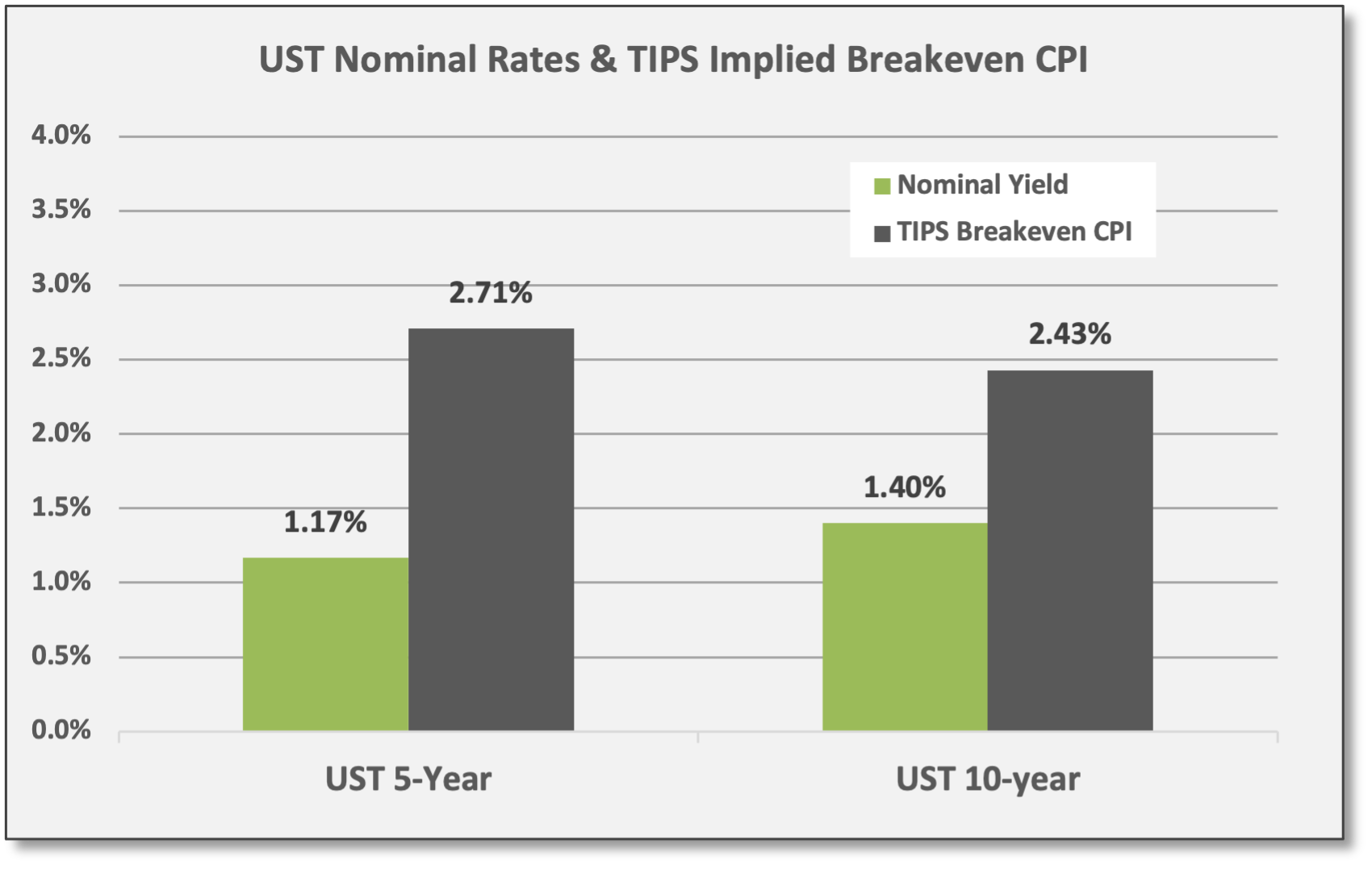

Inflation expectations have declined in recent weeks, based on market-pricing for nominal USTs and inflation-protected bonds. Breakeven yields show an implied inflation forecast of 2.7% over the next five years, matching the Fed’s core inflation forecast for 2022.

US/Global Equities

Defensive/yield-oriented equities outperformed with POSITIVE returns last week, but cyclical/value and secular/growth sectors declined. (Notice the green-shaded bars in the weekly performance graph.)

Staples (XLP), Utilities (XLU), Healthcare (XLV), and Real Estate (XLRE) delivered gains of 1.4%, 1.2%, 2.5%, and 1.8%, respectively.

Economic cyclicals Energy (XLE), Industrials (XLI), and Financials (XLF) declined -5.0%, -2.8%, and -1.2%.

Long-duration secular growth saw valuation compression with Technology (XLK) and Consumer Discretionary (XLY) down -4.0% and -4.7%, respectively.

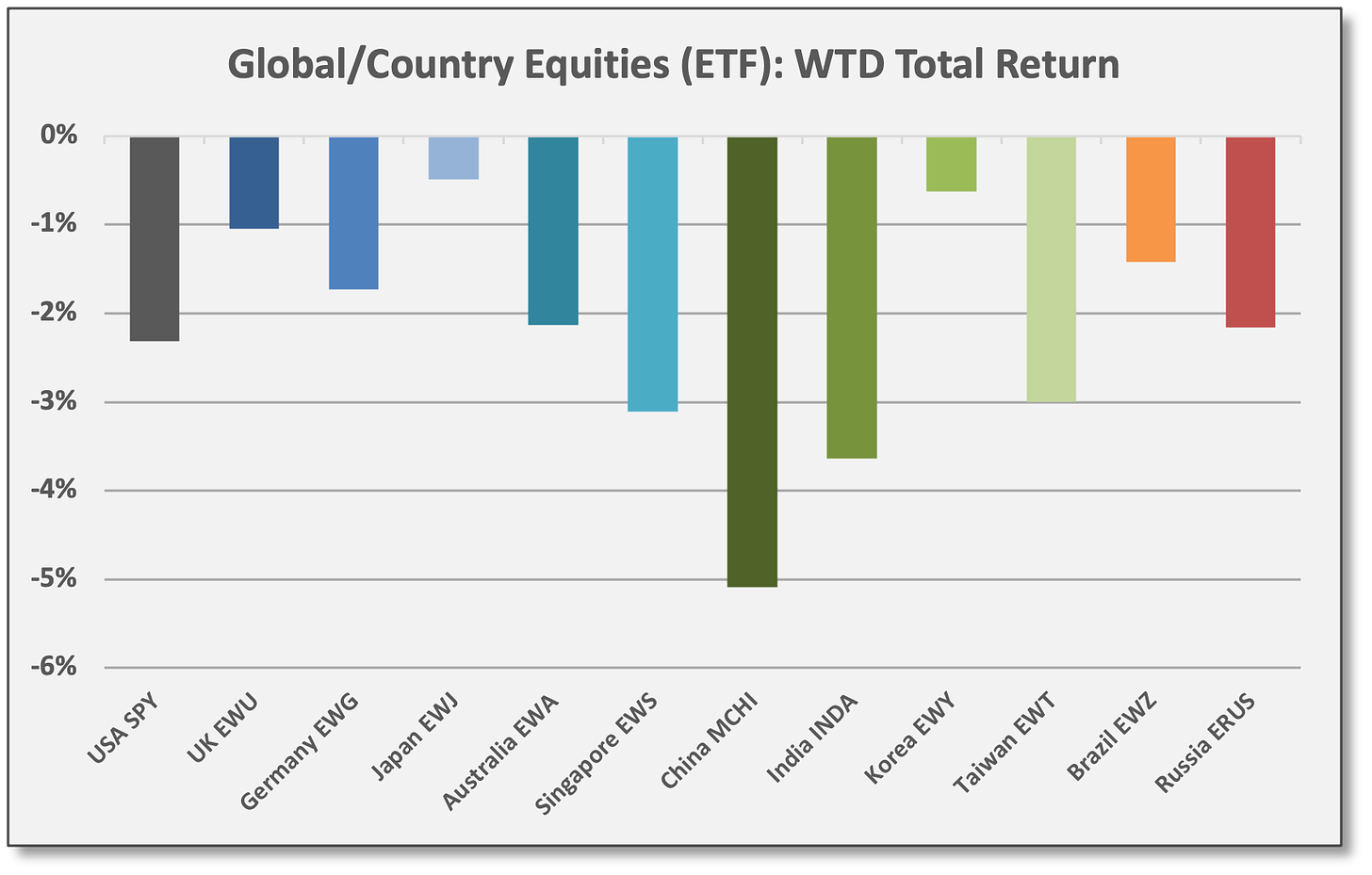

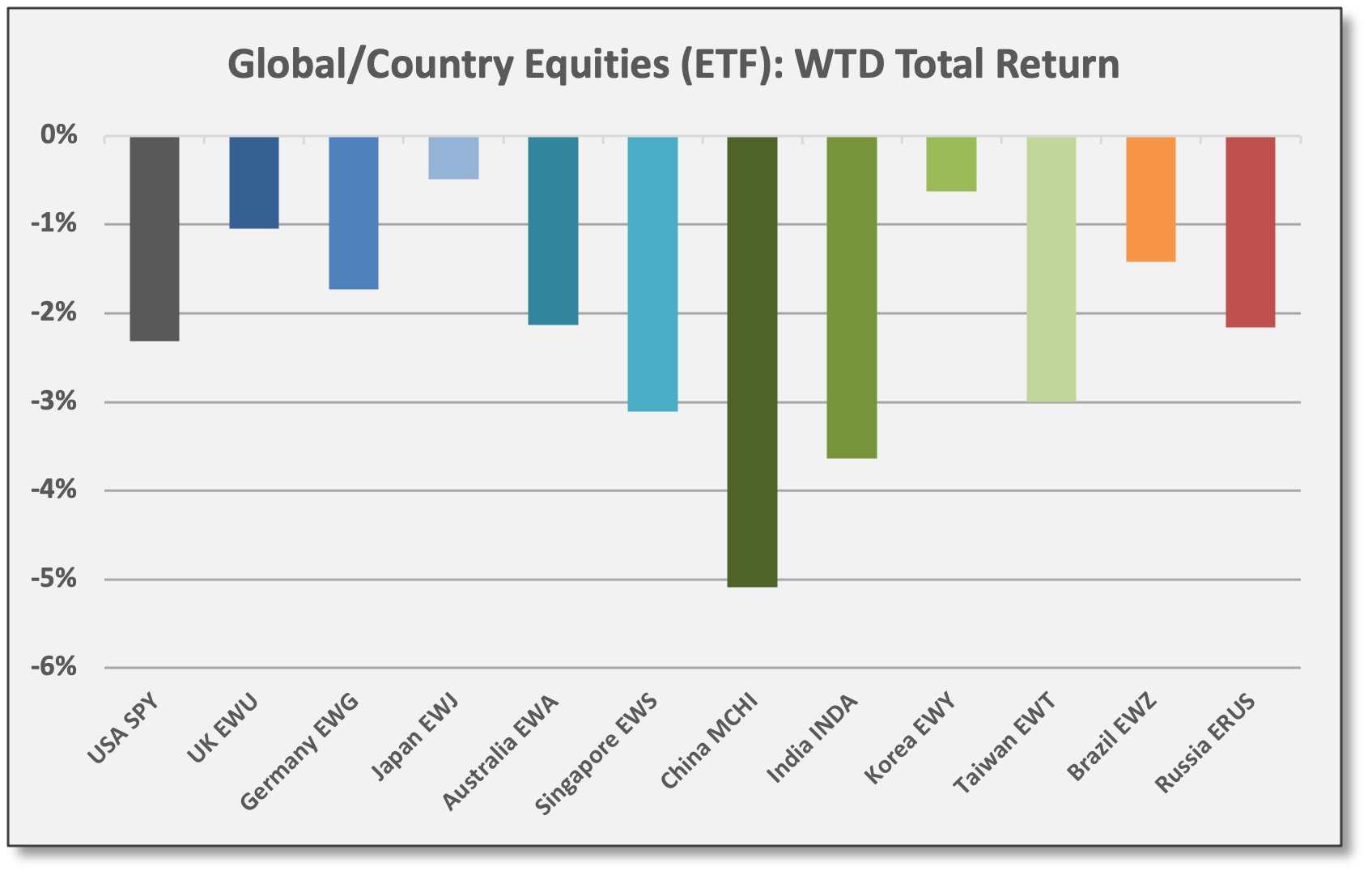

For non-US markets, it was losses across the board last week. No further commentary is needed.

Sources: CCM, Koyfin

Sources: CCM, Koyfin

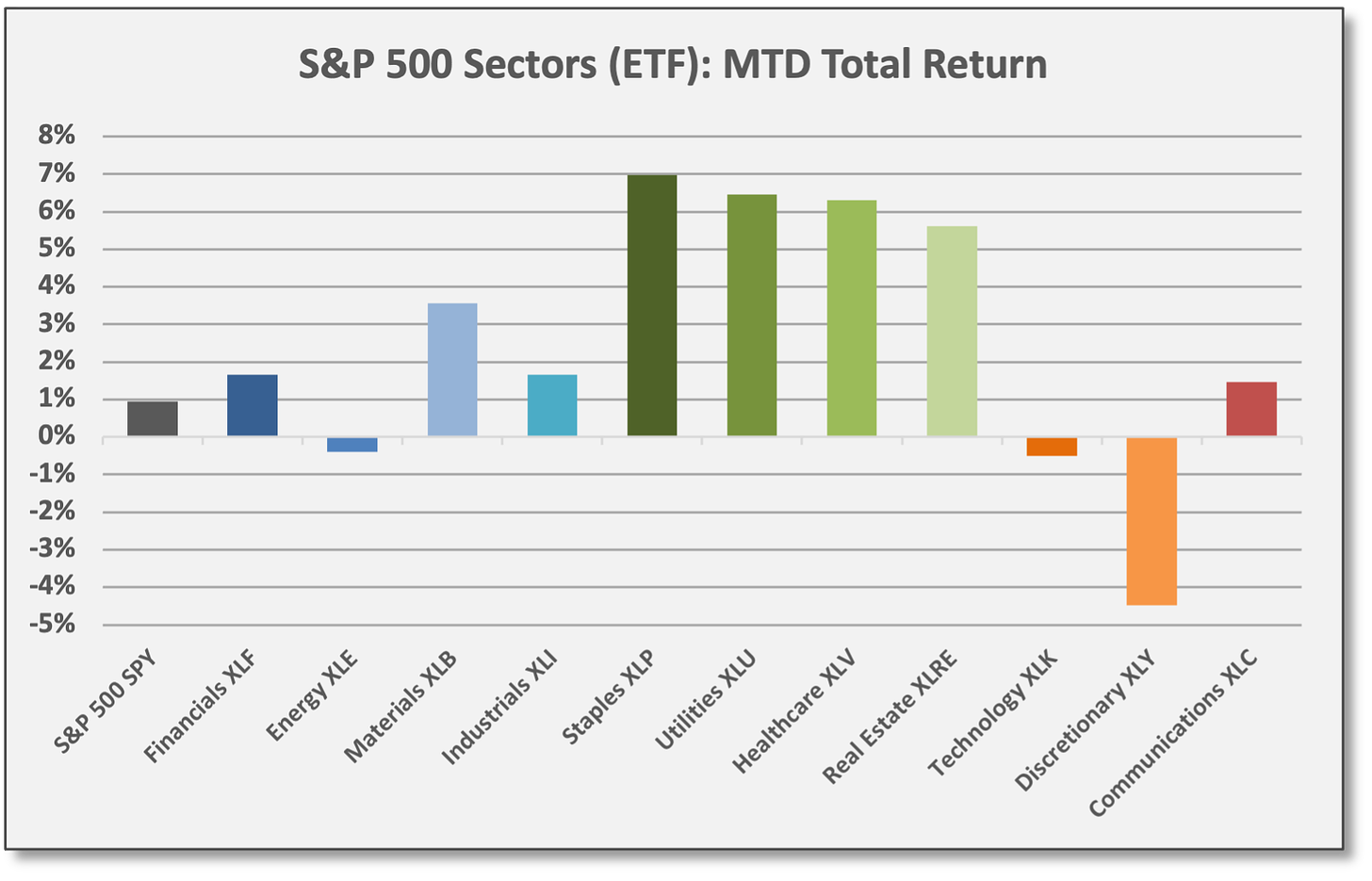

For December: Defensive/yield-oriented sectors have substantially outperformed.

Leaders for the month have been the steady, slow-growth, dividend-oriented sectors. Staples (XLP) are outperforming with a gain of 7.0% followed by Utilities (XLU) at 6.5% and Healthcare (XLV) at 6.3%.

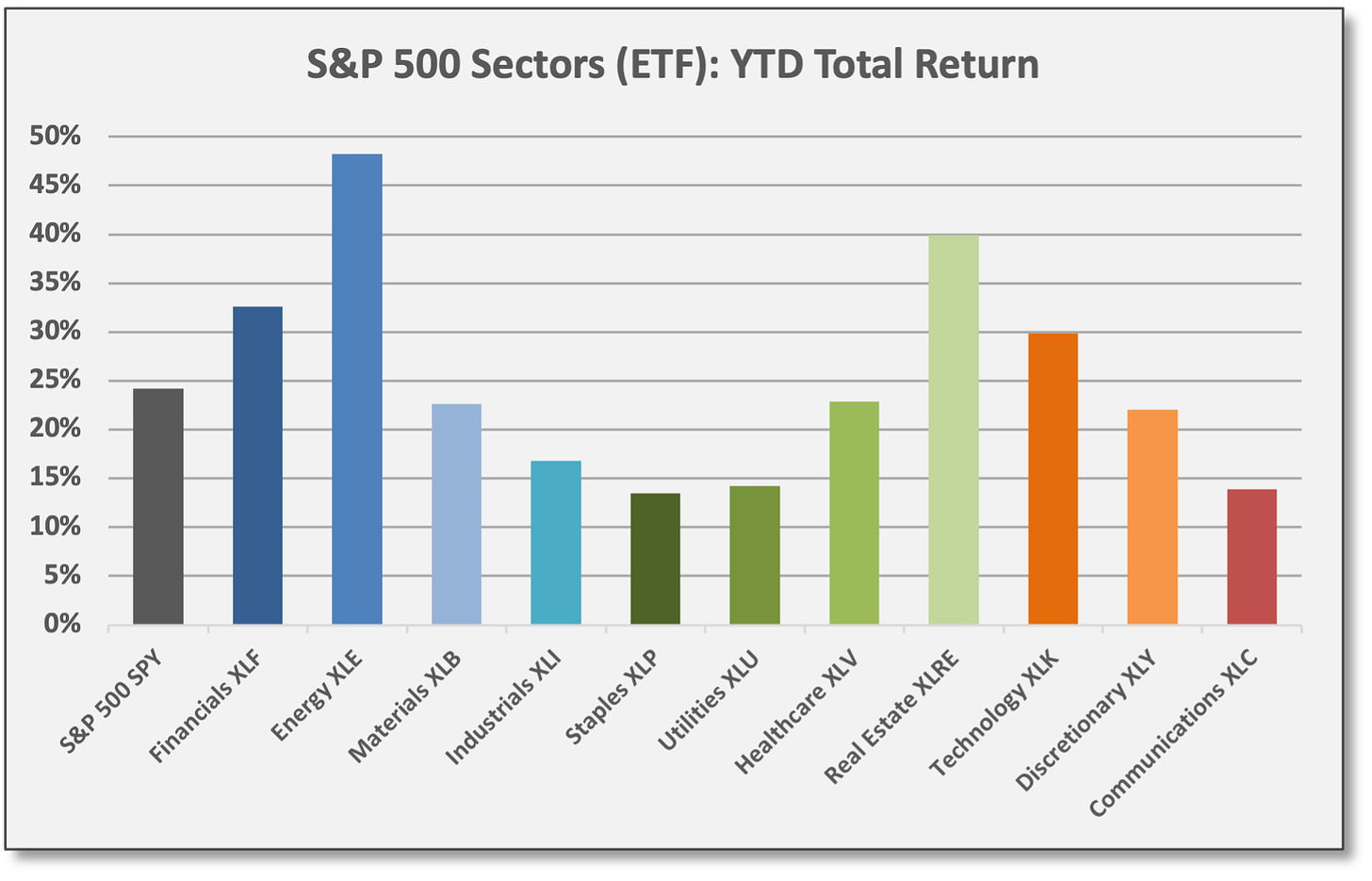

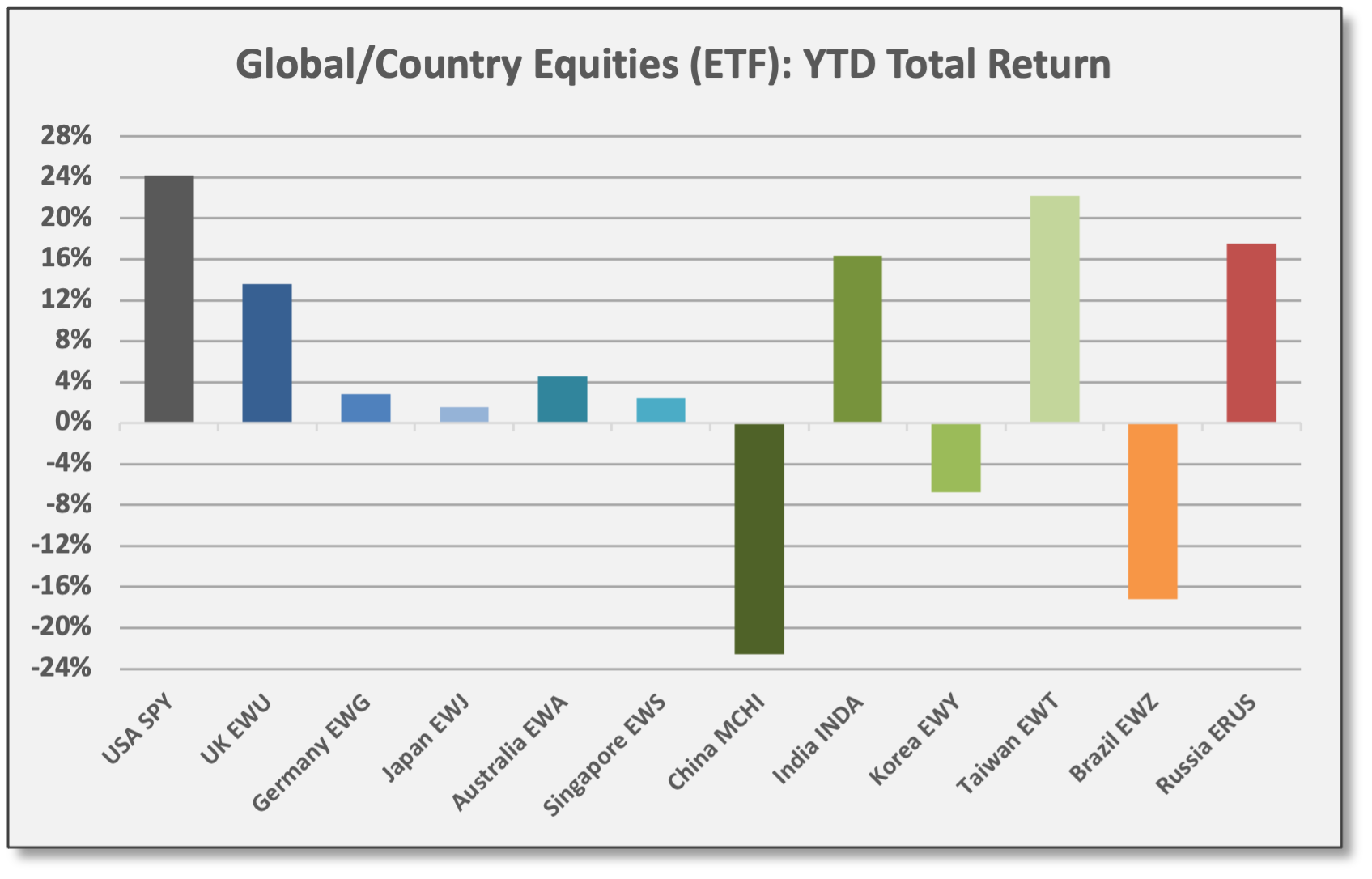

Cyclical/value sectors and secular growth have lagged for December, despite showing outperformance for 2022.

Sources: CCM, Koyfin

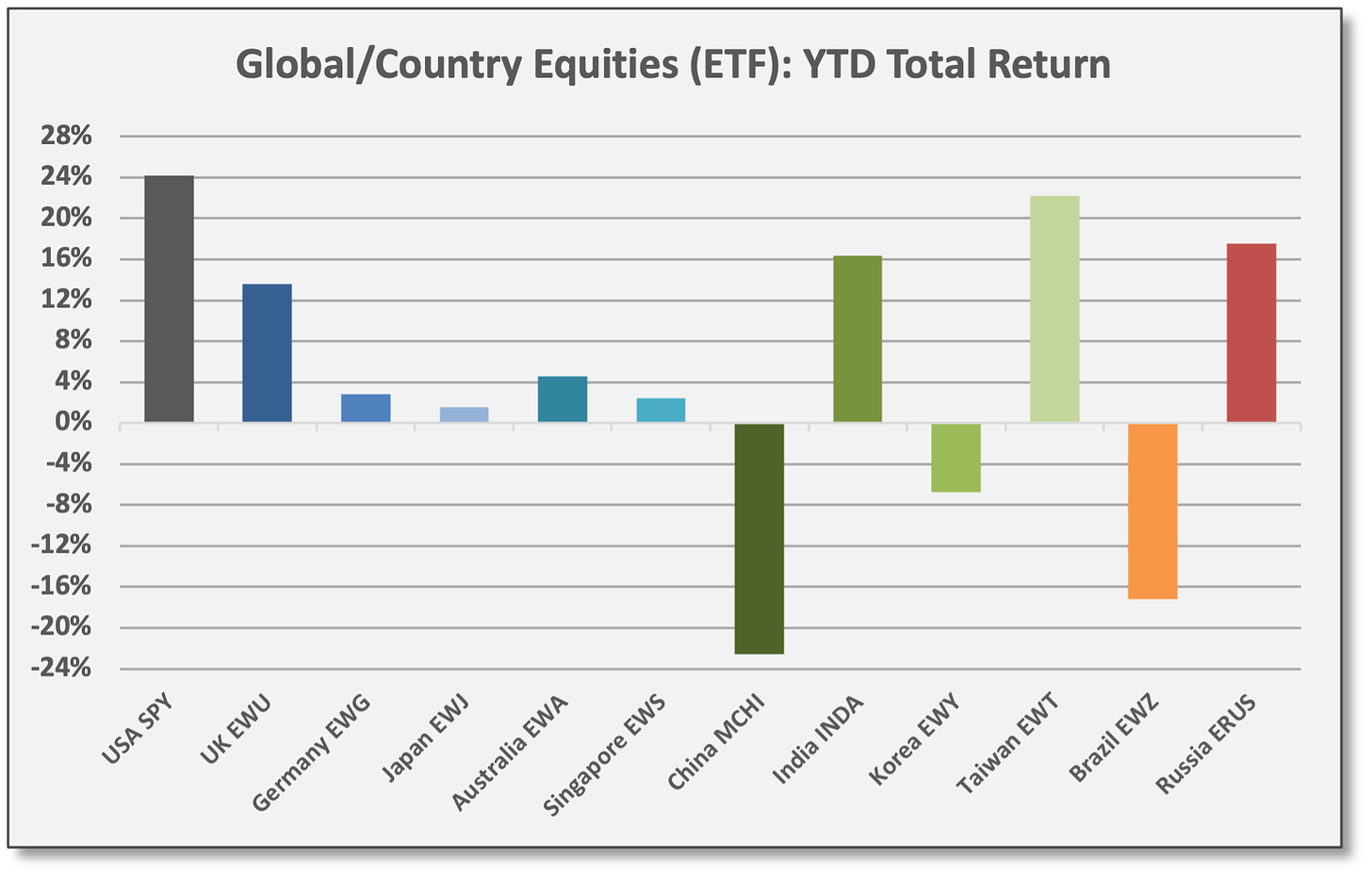

Sources: CCM, Koyfin For non-US equities, December performance has been mixed.

Mostly positive returns for Developed Markets, but Emerging Markets are showing wide dispersion.

Sources: CCM, Koyfin

Sources: CCM, Koyfin

Comparing Dividend Yields: As mentioned above, defensive/dividend-oriented sectors have outperformed so far this month. Sectors perceived as traditional income producers have outperformed with current dividend yields listed below. Real Estate and Utilities are among the top dividend yields followed by defensive Staples.

Perhaps surprisingly, Energy is the top-yielding sector, although yields are down from the “stressed” levels of a year ago. Exxon Mobil (XOM) and Chevron (CVX) offer dividend yields of 5.9% and 4.7%, respectively. Both companies have defended their dividends and operate as “unloved cash machines” as Forbes suggested last year.

Profits for the S&P 500 Index are projected to increase 8-9% in 2022 based on consensus estimates from equity analysts. EPS growth estimates for next year are segmented by sector below.

Commodities & Real Assets

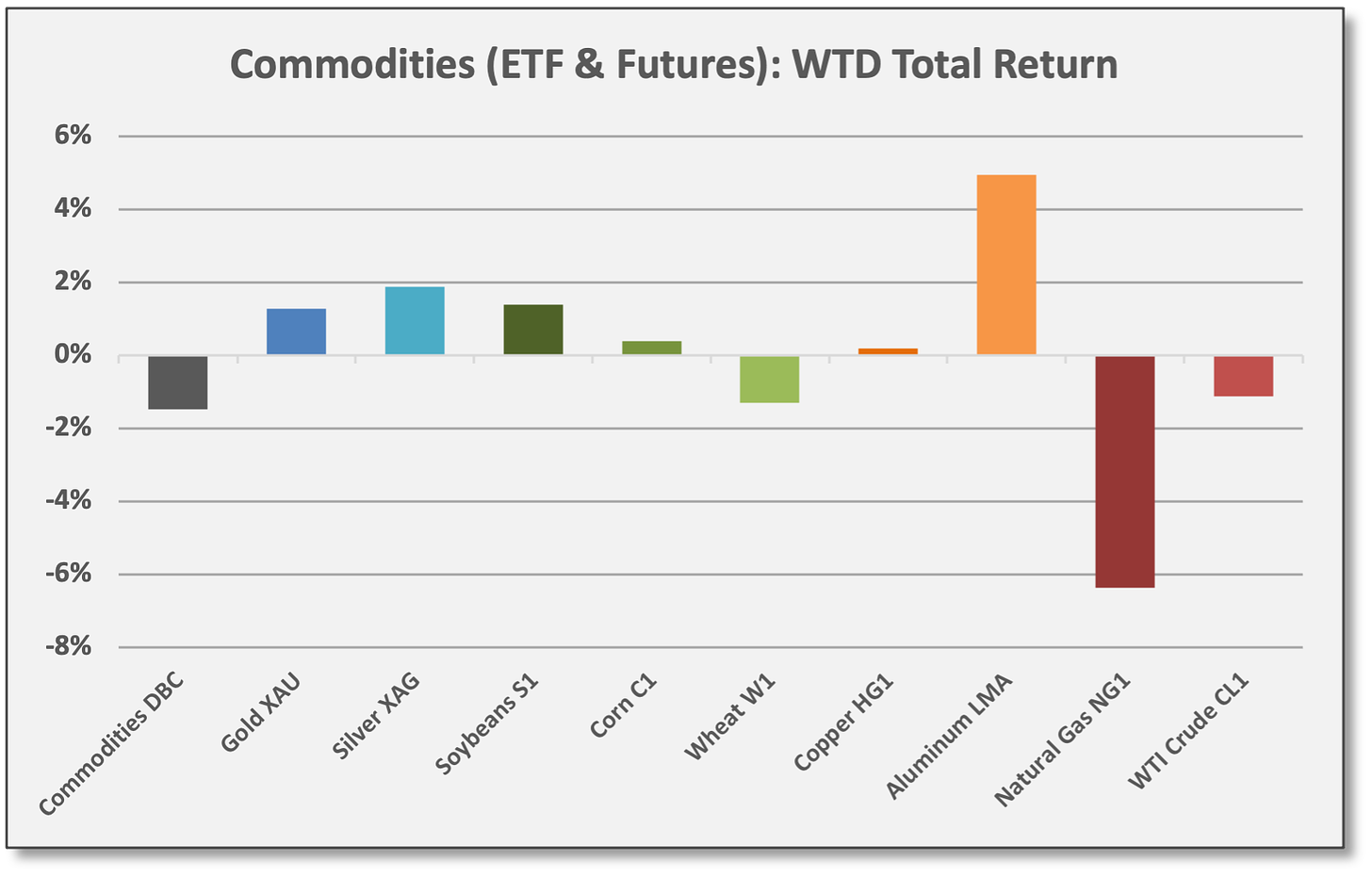

Base Metals and Precious Metals have opposite behavioral perceptions, but both gained last week.

Base Metals (DBB) — viewed as economic-sensitive cyclicals — gained 1.8%. Aluminum (LMA) rallied 5.0%.

In a risk-off market, Gold (XAU) and Silver (XAG) delivered safe-haven gains of 1.3% and 1.9%, respectively.

Sources: CCM, Koyfin

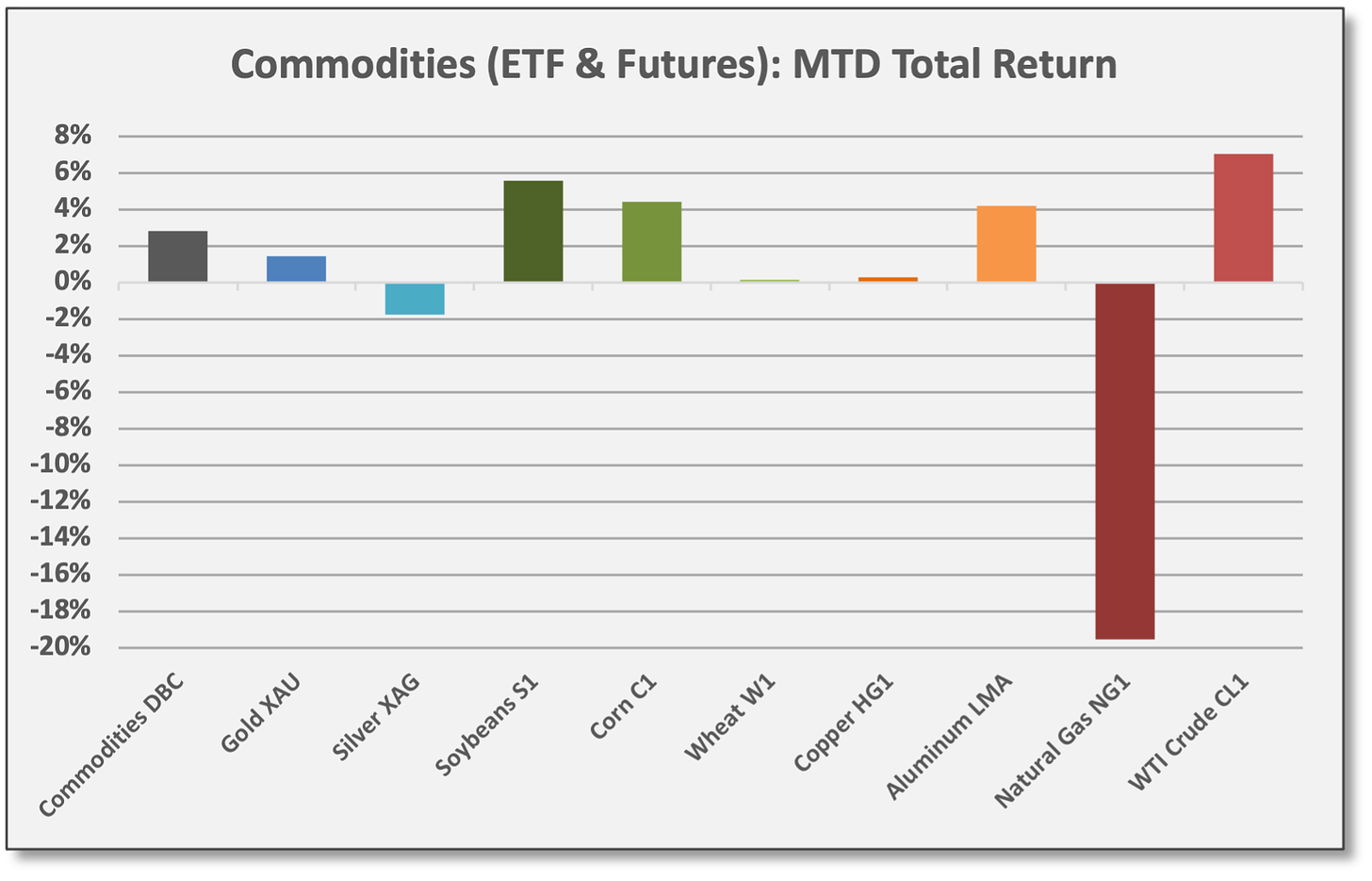

For December: All four sectors are positive with volatile energy commodities leading the way.

Diversified commodities (DBC) are up 2.8% for December.

Energy (DBE) is up 4.4%. WTI Crude (CL1) is up 7.1%, but Natural Gas (NG1) has plunged -19.5%. Energy and Base Metals also are the top performers for 2022, benefiting from the global demand recovery and undersupplied markets.

Agriculture commodities have been lifted by Soybeans (S1) and Corn (C1) this month with gains of 5.6% and 4.5%, respectively.

Aside from last week, Precious Metals continue to lag and are failing to deliver meaningful “inflation hedge” attributes.

Sources: CCM, Koyfin

Sources: CCM, Koyfin

Volatility, Flows/Positioning & Sentiment

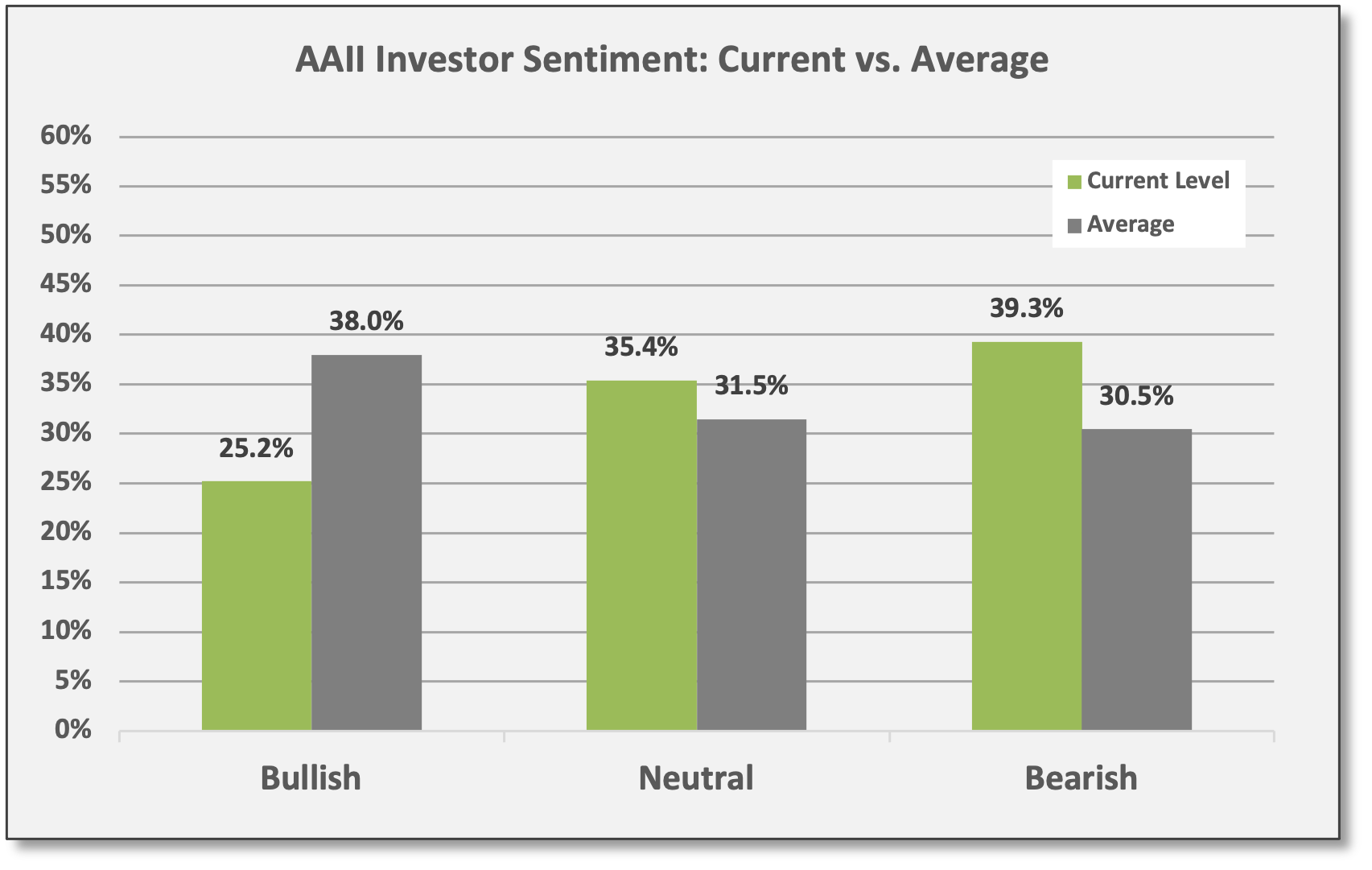

Investor sentiment declined last week. Bullish sentiment is below average and bearish sentiment is above. Normally, such sentiment is viewed as a contrarian indicator — so the bearish views could portend positive equity returns in the near-term.

Omicron coverage might be contributing weak sentiment, but inflation seems to be a larger factor. Bespoke and others have circled inflation as the main factor driving consumer confidence lower. Moreover, the NFIB small-business survey flagged inflation as a rising problem. Again, all this helps explain the policy pivot by Democrats who decided to delay legislative initiatives (Build Back Better) which are viewed as inflationary.

Implied volatility (VIX) fluctuated up and down last week within a range, but remains lower versus the panic selling that engulfed markets at the beginning of the month when Omicron headlines were first emerging.

“Short gamma, poor liquidity and extremely stressed VIX space exaggerated all moves. The crowd has de-grossed quickly and VIX is relatively well bid again.” The Market Ear, 12/14/21

The Market Ear summarized as follows: “SPX managed shaking out a lot of people over the past weeks. Short gamma, poor liquidity and extremely stressed VIX space exaggerated all moves. The crowd has de-grossed quickly and VIX is relatively well bid again. Obviously, there is an FOMC VIX premium priced in, but how big should it be... or is the crowd hedging something else?”

Portfolio Construction & Trading Ideas

JPMorgan’s Kolanovic expects a cyclical/value rally into year-end. Marko Kolanovic is a quant-based research expert. He is well respected for his for his data-oriented market views. Kolanovic issued commentary on 12/17.

Kolanovic noted the recent sell-off in small-cap, high-beta, and value-oriented equities in recent weeks.

He highlighted a “divergence” between index returns and median stock performance. For instance, the Russell 3000 (IWV) is up 21.8% for 2022, but the median return across the ~3000 underlying holdings is 14.7%.

Specifically, Kolanovic referenced declines for single-name equities versus their 2022 highs. For instance, the “average” stock in the Russell 3000 is down ~28% from highs earlier this year; the “median” stock is down ~21% from highs.

Considering the Russell 3000 is up ~22% for the year with so many stocks down over 20% from their highs, some strategists might view this as a negative signal — narrow leadership — but Kolanovic sees the “divergence” in a more favorable light.

Kolanovic believes short-selling and other technical positioning explains the peculiar divergence and sees a rebound setting up.

“Such a divergence is unknown to us, and indicates a historically unprecedented overshoot in selling smaller, more volatile, typically value and cyclical stocks in the last four weeks. The narrative for the sell-off is related to Omicron and the Fed, while actual selling comes largely from de-risking and shorting from equity/macro hedge funds. For short-selling campaigns to succeed, there have to be positioning, liquidity, and often systematic amplifiers of the sell-off. We believe these conditions are not met, and hence this market episode may end up in a short squeeze and cyclical rally into year-end and January.”

“One should note that large short positions likely need to be closed before (the seasonally strong) January, which is likely to see a small-cap, value, and cyclical rally…” Marko Kolanovic, JPMorgan, 12/17/21

Kolanovic reviewed institutional and retail positioning and other technical/flow-based factors. He detailed the downsizing and “de-grossing” of portfolios by leveraged hedge funds and other volatility-oriented strategies like risk-parity funds, suggesting that much of the selling has run its course. In all, Kolanovic concludes that short-positioning is overextended.

“Yet, there is aggressive shorting, likely in a hope of declines in retail equity positions and cryptocurrency holdings — while in fact both of these markets and retail investors have shown resilience in the past weeks. One should note that large short positions likely need to be closed before (the seasonally strong) January, which is likely to see a small-cap, value, and cyclical rally. And given that market liquidity is dwindling, the impact of closing shorts may be bigger than the impact of opening them, when liquidity conditions were better.”

“Omicron’s mortality rate is very low... This is consistent with Omicron being a bullish rather than bearish market development.” Marko Kolanovic, JPMorgan, 12/17/21

Finally, in terms of addressing the macro risk getting so much attention from media and policymakers, Kolanovic shared his latest perspectives on the virus. “On the macro fundamental side — we retain our positive outlook for COVID. Despite the recent panic about the Omicron variant, global COVID deaths are at the lowest point of the year, and cases actually [are] flat for the past two weeks... Omicron’s mortality rate is very low... This is consistent with Omicron being a bullish rather than bearish market development.”

What Others Are Saying

The Bespoke Report, 12/17/21: “Economic data lately has generally been coming in better than expected and the Fed’s actions this week suggest that they are confident the recovery will continue. However, there are a number of crosscurrents. With inflation at multi-decade highs and income growth not keeping pace, consumer sentiment has been unusually weak. Furthermore, the Omicron variant is now running rampant in the US as New York State just reported a record single-day number of new COVID cases. While it appears as though this variant is much less severe than other strains, it’s still having a big short-term impact with new rounds of closures and activity restrictions... investors have turned pretty bearish as well, and it’s showing up in the stocks that have been outperforming. Consumer Staples has been one of the top performing sectors this month… That’s not the type of performance you typically see from a market expecting strong economic growth, but then again, the negative sentiment and sharp rallies in the most defensive areas of the market hardly indicate complacency.”

Christopher Wood, Head of Global Equities, Jefferies, 12/16/21: "GREED & fear still has a very hard time seeing the current Fed leadership ever becoming really hawkish. But the current leadership is, unlike Paul Volcker, highly political in nature. And the growing political pressure raises the risk that the Fed acts more hawkishly in the nearer term than GREED & fear had previously expected until a major risk-off move causes them to move the other way. It should also be born in mind that the current focus in Washington is on when the Senate will pass the bizarrely named ‘Build Back Better’ legislation which could add as much as $5 trillion of spending based on the latest Congressional Budget Office (CBO) estimate… The political reality is that this legislation is going to be criticized by Republicans not only for being un-American and socialist, in terms of its promotion of European-style welfarism, but also for fanning inflation.”

Aneta Markowska, Chief Economist, Jefferies, 12/13/21: “The JEF US Economic Activity Index rose by 1.9 points last week to 104.1. The index is up 2.4 points in the last four weeks, and has remained above 100 for more than a month. Last week's bounce confirms that the previous volatility was related to seasonal swings around Thanksgiving, and NOT due to Omicron. While the variant poses an obvious downside risk for Q1, it's hard to point to any visible impact on activity so far.”

Raymond James, Portfolio Strategy, 12/16/21: “The Fed’s hawkish pivot is prudent in our view with very loose financial conditions and elevated inflation. The Fed revised its 2022 GDP estimate to 4% growth, 2.6% core inflation, and 3.5% unemployment rate — a solid economic backdrop should it prove accurate. That said, given that the Fed has been so important to equity markets since the credit crisis, a normalization of policy (and more hawkish pivot) could come with more moderate returns and normal volatility/choppiness over the next 3-6 months... The S&P 500 has been basing since early November. And beneath the surface lately, there has been some defensive rotation... We have a bias for the Fed’s hawkish pivot to be a headwind for appreciably higher equity prices and may result in more range-bound trading. Basing may continue, but positive seasonal factors, along with a healthy macro [environment] and overall earnings growth supports accumulating when the market is near technical support or if a deeper decline (normal pull-back) develops.”

BofA Securities, The Flow Show, 12/16/21: “Inflation always precedes recessions: Whether driven by asset, housing, commodity, consumer, or labor, inflation is like a very high body temperature, and must be reduced via tightening or recession to return the body to normal and ensure future good health… Global growth [is] good right now [despite Omicron risks] but with [so few] investors forecasting recession in '22, risk that [a] ‘rates shock’ quickly morphs into [a] ‘recession scare’ is high… We remain defensive and bearish until positioning shows full-blown capitulation and/or credit events/losses on Wall Street force central banks to announce [a] reversal of tightening.”

David Zervos, Chief Market Strategist, Jefferies, 12/19/21: “The notion that the Fed is way behind the curve, that they have made a colossal mistake by remaining too accommodative for too long, and that they have lost all of their hard-won inflation-fighting credibility, could not be further from the market-implied truth. Financial asset prices are fully embracing the notion that our current CPI inflation spike to 6.8% is nothing more than a short-term disruption, emanating largely from supply-side constraints… Longer-term yields and forward breakevens should continue to shun the permanent-inflation scaremongering narrative, but as the Fed falls for this sham storyline, a policy mistake-driven trading opportunity arises in both [the S&P 500] and the short-end of the [UST] yield curve.”

It’s the Holiday Season. Consider giving a Coffee & Capital Markets gift subscription to:

Clients — to keep them alert to relevant data and trends

Colleagues and team members who need to leverage their time

Students or young up-and-comers who thrive on learning

Seasoned investors looking to keep an edge

Family members who follow the markets

This material is for informational and educational purposes only. All data has been compiled from sources believed to be reliable, but there is no guarantee of its complete accuracy.

The “central tendency” range eliminates the high/low outlier estimates.

Personal Consumption Expenditures, reported by the Bureau of Economic Analysis. The November report is set for 12/23/21.

FOMC is set to meet on May 3-4, 2022.